The digital ecosystem in Bangladesh, specifically within the agency-dense clusters of Dhaka’s Gulshan, Banani, and Uttara sectors, presents a marketplace defined by a massive gap between operational volume and strategic authority. An audit of 28 prominent agencies reveals a sector struggling with “Generalist Dilution,” where technical fulfillment is abundant but unique strategic mechanisms are rare. With performance scores spanning a wide range from a floor of 42 to a ceiling of 84, the data suggests that for most firms, brand messaging acts as a conversion leak rather than a growth engine.

Quantitative Landscape and Performance Tiers

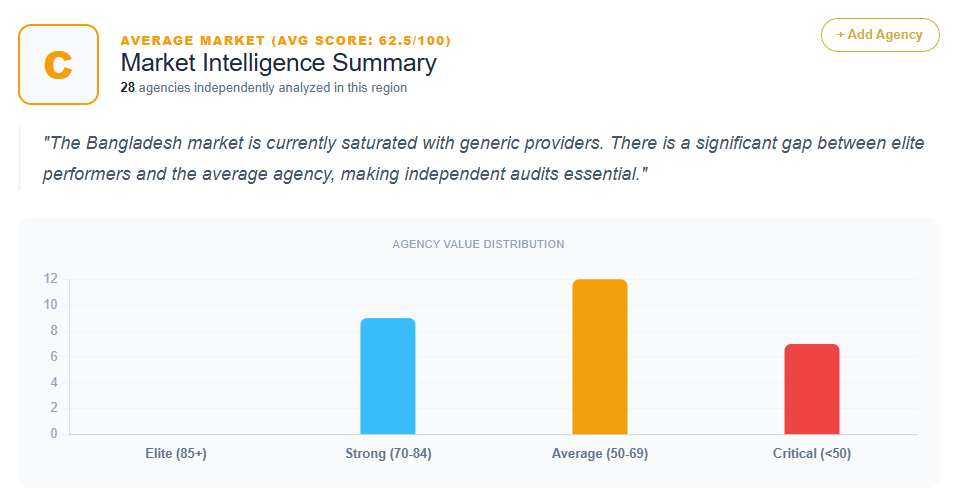

Across the 28 analyzed providers, the distribution of scores highlights a market plateau. Only two agencies, UpGraph (84) and One Little Web (82), have successfully broken into the 80+ tier. These outliers share a common trait: hyper-specialization in niche global markets like SaaS, B2B, or international link building.

The remainder of the market is divided into three distinct segments:

- The Premium Generalists (Scores 72–74): Comprising 21% of the dataset (6 agencies including Viser X, Khan IT, Geeky Social, Magnito Digital, Analyzen, and Webable Digital). These firms possess high-tier visual branding and local prestige but are consistently diagnosed with “Generic Excellence Syndrome.”

- The Mid-Tier Commodity Zone (Scores 58–68): This is the most saturated segment, representing 39% of the market. Agencies like Bizcope, Notionhive, Ecomclips, and DigitalWit offer functional services but lack the “strategic teeth” to command premium market share against specialized entrants.

- The Legacy IT Utilities (Scores 42–48): Making up 25% of the market, firms such as Enterprise 360, Dhrubok Infotech, TechnoBD, and Orbit Informatics treat SEO as a secondary add-on to hosting, graphics, or general BPO, leading to “Generalist Fatigue” and low strategic depth.

The “Generalist Trap” and the Failure of All-in-One Positioning

A recurring friction point across 75% of the agencies scoring below 70 is the attempt to be a “one-stop shop.” The diagnostic data indicates that this “Jack-of-all-trades” approach is the primary driver of strategic misalignment.

For agencies like Enterprise 360 (42) and Dhrubok Infotech (42), the value proposition is centered on a broad catalog of features—Graphics, Web, and SEO—rather than specific business outcomes. This creates a “Generalist Dilution” where sophisticated enterprise clients perceive the firm as a commodity vendor rather than a strategic partner. This pattern persists even in larger firms; MonsterClaw LLC (74) is diagnosed with “All-Rounder Syndrome,” attempting to address Affiliate, SEO, and B2B Lead Gen simultaneously, which dilutes the authority required to dominate the technical SEO niche.

Creative-First Strategic Misalignment

In the premium corridors of Banani and Gulshan, a specific “Creative-First” bias emerges. Notionhive (68), Magnito Digital (72), and Webable Digital (72) lead with brand aesthetics and storytelling. However, the analysis shows that this “Innovation and Strategy” narrative creates a gap in perceived technical depth. Specifically, Webable’s “Simple. Smart. Social.” identity, while effective for social media, acts as a barrier to technical SEO procurement, as search dominance requires a clinical, data-first messaging framework that creative-heavy agencies currently omit.

Competitive Benchmarking: Local Dominance vs. Global Anonymity

The benchmarking data reveals a tension between deep-rooted local agencies and “faceless” global entities.

- Local Trust as a Moat: Analyzen (74) and Magnito Digital (72) leverage their status as legacy pioneers (Analyzen being the first ever digital agency in Bangladesh) to win blue-chip clients like Grameenphone and City Bank. However, they consistently lag behind niche specialists in demonstrating granular, SEO-specific technical methodology.

- The Localization Barrier: Global providers like eIntelligence (45) and SEO Audit Agency (58) lack physical presence or cultural integration in Bangladesh. Their “one-size-fits-all” templates fail to address bilingual search intent or local payment logistics, resulting in a 50–70% drop-off in the middle of their conversion funnels when targeting the Bangladesh market.

- The Export Outliers: One Little Web (82) and UpGraph (84) have moved away from the “Local Partner” sentiment to focus on global SaaS and B2B markets. While they offer superior editorial standards, they face a “Global vs. Local” friction that makes them feel over-engineered for domestic-only BD conglomerates.

Quantifying the ROI of Strategic Brand Weakness

Generic messaging is not merely a creative failure; it is a measurable financial liability. The diagnostic data provides several specific ROI leakage points:

- Lead-to-Close Ratio Penalties: Agencies like Viser X, Khan IT, and IMBD Agency likely experience a 15–30% lower lead-to-close ratio for enterprise-level clients who prioritize specialized expertise over generalist capacity.

- Conversion Funnel Leakage: For eIntelligence, the lack of localized trust signals likely results in a 50–70% loss of targeted leads. Similarly, Digital Solutions IT (48) faces a 40–50% loss in potential high-ticket conversions due to a “service catalog” approach that sophisticated buyers bypass.

- The Commodity Tax: For firms like Flyte Solutions (62) and Roopokar Creative Studio (48), the focus on “Creative Digital” or “Creative Studio” branding attracts low-margin clients seeking execution rather than strategy, potentially costing these agencies 25–35% in annual recurring revenue (ARR) growth.

- Customer Acquisition Costs (CAC): The “Trust Deficit” created by generic positioning—noted in the profile for SEO Audit Agency (58)—results in a 40–50% higher CAC compared to agencies that lead with localized social proof and industry-specific outcomes.

Strategic Prescriptions: From Execution House to Strategic Partner

The data outlines a clear path for agencies to break out of the commodity cycle and reclaim lost margins. The common thread among all prescriptions is the move from “Selling Hours” to “Selling Systems.”

Productization of Intellectual Property

Nearly all mid-to-low tier agencies are advised to transition from “Service-Based” to “Mechanism-Based” headlines. The diagnosis suggests that agencies must develop proprietary methodologies to move from commodity to consultant status. By branding their execution models—such as the proposed “Viser-X Alpha Framework” or the “EX-Index Growth Map”—firms create “Perceived Uniqueness” that justifies premium pricing and reduces price-based competition.

Verticalization for Sector Authority

The analysis identifies a significant gap in sector-specific authority within the Bangladesh market. Agencies are urged to deploy specialized landing pages for the country’s high-growth industries, specifically Ready-Made Garments (RMG) export, Fintech, Real Estate, and E-commerce. Freelance Topic (58) and Enterprise 360 (42) are specifically prescribed to build “Local Dominance” playbooks for these sectors to move away from the “freelancer nomenclature” that creates a cognitive ceiling for corporate clients.

Pivot to Outcome-Driven Narratives

The market’s highest performers win by leading with “Revenue and Rankings” KPIs rather than “Innovation and Strategy.” The data suggests that agencies like Ecomclips (68) and DigitalWit (68) must pivot from “what we do” to the “Economic Impact” of their interventions. This involves integrating high-visibility social proof—such as specific growth percentages for recognized Bangladeshi brands—directly above the fold to solve the “Trust gap.”

Conclusion: The Opportunity for Strategic Disruption

The Bangladesh SEO market is characterized by high technical competence but low strategic differentiation. With an average score of 63.8, the 28 agencies analyzed are largely trapped in a “Utility Brand” mold. While technical infrastructure is a given, the lack of proprietary methodology and industry-specific verticalization is costing the majority of these firms between 15% and 50% of their potential lead value. As highlighted by the niche dominance of UpGraph and One Little Web, the future of the market belongs to the specialized growth architects who can bridge the gap between technical execution and quantifiable business cash flow. For the remaining 26 providers, the path to market leadership requires a radical abandonment of the “one-stop-shop” identity in favor of data-driven, mechanism-led authority.

Get Your SEO Strategy