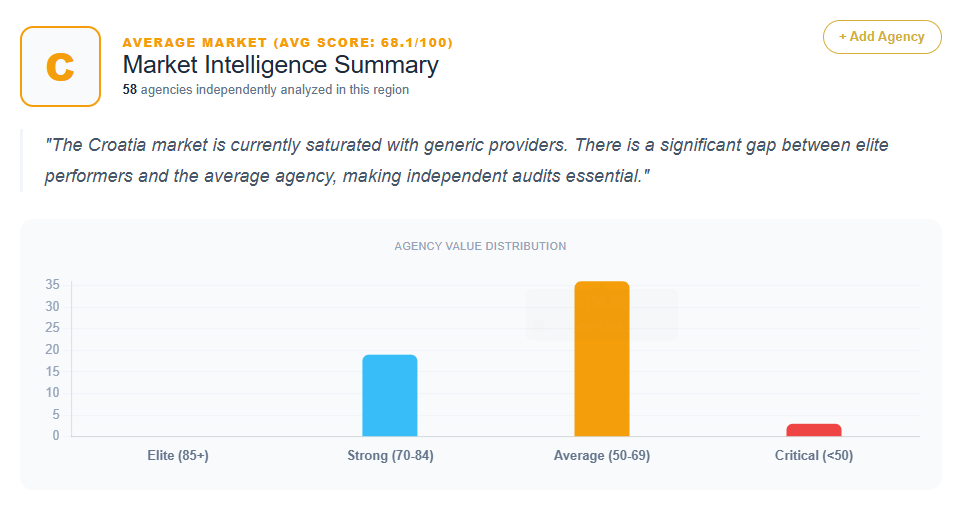

An exhaustive analysis of 58 SEO agencies operating within Croatia—ranging from the high-authority corporate hubs in Zagreb to regional clusters in Osijek, Split, Pula, and Rijeka—reveals a market defined by high technical capability but a profound deficit in strategic “Only-ness.” While the technical floor of the Croatian market is remarkably solid, the diagnostic data suggests that the majority of providers struggle with what is frequently identified as the “Generalist Trap” or “Commodity Fatigue.”

The quantitative data provided indicates a broad performance spectrum. Scores across the 58 analyzed entities range from a market high of 84 (404 Agency) to a low of 42 (Intersoft d.o.o.). A significant portion of the market—approximately 65% of the analyzed group—is clustered between the scores of 62 and 68. This suggests a “Sea of Sameness” where agencies meet basic operational requirements but fail to provide a unique strategic reason for high-value enterprise selection.

The Performance Hierarchy: Analyzing the Scoring Clusters

The Croatian SEO market is tiered based on its ability to bridge the gap between “technical tasks” and “business outcomes.”

The “Alpha” Tier (Scores 80–84)

Only a handful of agencies achieve scores above 80. 404 Agency (84) leads the market, leveraging its stature as a communications powerhouse. However, even at this level, the agency is diagnosed with “Strategic Misalignment,” as its SEO messaging is often buried under general PR and communication narratives. Degordian (82) and Arbona (82) represent the high-tier integrated and performance sectors, yet both are penalized for “Generalist Dilution,” where their broad service portfolios obscure their specific technical SEO depth. Logit (82) and Inchoo (82) represent the specialized “Authority” tier, winning on B2B strategy and eCommerce architecture, respectively. Escape Digital Agency (82) rounds out this tier, though its SEO value is noted as being occasionally overshadowed by its dominant PPC reputation.

The Mid-Market Contenders (Scores 70–79)

This bracket includes SeekandHit (78), Markething (78), Point Visible (78), Fokus (78), Marker (78), Kontra (76), Lloyds Digital (74), KG Media (74), Gauss Development (74), Link Digital (74), In Rebus (72), and Studio 22 (72). These agencies are professionally stable but often suffer from “Premium Generalism.” For instance, Lloyds Digital is a leader in technical execution but is cautioned that its brand strength in development “overshadows” its marketing expertise, creating a perception of being a generalist in growth strategy.

The “Generalist” and Regional Tier (Scores 42–69)

The largest segment of the market scores below 70. This includes firms like Grafikart (68), Creative Media (68), Idea Studio (64), and Spona Digital (64). These firms are consistently diagnosed with “Commodity Trap” syndrome. Their value propositions rely on generic industry jargon like “digital solutions” or “your partner for growth,” which are described as “table stakes” rather than differentiators. The bottom tier, featuring Intersoft (42), Netcom (48), and Web Dizajn (48), is characterized by “Service-Centric Inertia,” where SEO is positioned as a technical “add-on” to hosting or basic web maintenance.

Recurring Strategic Weaknesses: The Generalist Trap

The most prevalent diagnosis across the 58 agencies is “Generalist Dilution.” In the Croatian market, agencies frequently lead with a “Full-Service” narrative.

Creative vs. Technical Misalignment

Agencies such as Studio 33 (68), Kreativni laboratorij (64), and Fabula (68) are noted for prioritizing aesthetics or storytelling over the analytical rigor required for SEO dominance. The data suggests that this “Design-First” lead profile attracts clients with small budgets but fails to capture enterprise-level SEO contracts. For Kreativni laboratorij, this creative focus demotes SEO to a “tactical checkbox” rather than a strategic revenue driver.

Technical Myopia

Conversely, firms like Inchoo (82), Gauss Development (74), and Barrage (68) suffer from “Technical Myopia.” While their technical implementation is superior due to their development roots, they fail to articulate the business impact of this advantage. Inchoo, for instance, is viewed as a “development house first,” which weakens its positioning for pure-play SEO contracts among CMOs who prioritize market share over code stability.

Geographic Patterns: The Zagreb Hub vs. Regional Clusters

The physical location of an agency in Croatia significantly influences its competitive positioning and strategic flaws.

- Zagreb (The Competitive Epicenter): Home to 404 Agency, Degordian, and Kontra. Agencies here compete on “Institutional Credibility” but pay a “Doubt Tax,” as potential clients spend more time comparing prices because the value proposition isn’t uniquely articulated.

- Osijek (The Technical Powerhouse): Osijek features a massive cluster of providers including Escape, Inchoo, In Rebus, Gauss, Barrage, Ofir, Culex, Grafikart, Creative Media, Web-IT, Netvision, and Signum. While Osijek serves as a technical hub, the majority of its agencies are diagnosed with “Commodity Trap” messaging, selling “Visibility” instead of “Revenue.”

- The Adriatic Coast (Split, Rijeka, Pula, Zadar): Agencies here, such as Point Visible (Pula), SeekandHit (Split), and Multilink (Rijeka), often lean on regional trust. Point Visible is unique for its global B2B focus but is penalized for a “Distance Friction” that ignores the domestic Croatian market in its primary messaging.

Local Market Nuances: Tourism as a Specialized Moat

A unique Croatian market nuance is the dominance of the tourism and hospitality sector. Agencies like KG Media (74) and Lloyds Digital (74) successfully leverage this niche. However, KG Media is cautioned against “Legacy Dilution,” where historical strength in offline media planning overshadows its modern organic search authority. The data suggests that agencies that fail to explicitly define a “Hospitality SEO” framework are losing ground to specialized boutiques.

Quantifying the ROI of Strategic Misalignment

The financial consequences of poor differentiation are explicitly quantified in the dataset’s ROI notes for these 58 providers:

- Lower Conversion Rates: Generic messaging for firms like SeekandHit and Degordian results in a projected 15-20% lower conversion rate on specialized SEO inquiries.

- Lead Leakage: Agencies that do not quantify their impact through revenue-first messaging (e.g., Akvarij, WebLab) experience an estimated 20-30% leakage in potential lead conversion.

- The “Commodity Discount”: For mid-tier firms like Adlab and Signum, the lack of a “Strategic Hook” forces a “Commodity Discount” of 20-30% on potential retainers.

- Sales Cycle Inflation: Firms like Logit face a longer sales cycle (6-12 months) because prospects must consume significant content to understand the value, rather than being captured by a sharp, outcome-focused proprietary framework.

Prescriptions for Market Dominance: The Move to Productization

Across the 58 agencies, the prescriptions for growth are remarkably consistent. To move into the elite tier, Croatian providers are urged to rename and codify their internal processes. The dataset identifies several specific proposed proprietary frameworks:

- Search-First Brand Building (for Degordian)

- Data-Driven Search Intelligence (for SeekandHit)

- The Aras 360 Growth Blueprint (for Aras Digital)

- The Markething 360 Framework (for Markething)

- The Multilink Performance Matrix (for Multilink)

- The Adis Precision Audit (for Adis Digital)

- The V-Sync Growth Framework (for Studio V)

- Arbona Organic Intelligence Framework (for Arbona)

By shifting from selling “SEO services” (a commodity) to selling a “proprietary mechanism,” agencies move away from hourly-rate perception and justify premium pricing. Furthermore, the data recommends replacing generic headers with “Outcome-Based Value Statements” that focus on “Organic Market Share Domination” rather than just “Rankings.”

Conclusion: Strategic Outlook

The Croatia SEO market is technically mature but strategically underdeveloped. The industry is currently divided into “Integrated Giants” who are too broad and “Technical Dev-Shops” who are too narrow.

The data concludes that the path to market leadership in Croatia requires a total abandonment of generic “results-driven” language in favor of specialized, productized growth systems. Until the middle-tier agencies in Zagreb and Osijek stop listing features and start owning unique methodologies, they will continue to pay the “Genericness Tax” through lower margins and high client churn. In a saturated landscape, “Engineering-First Search Growth” and “Revenue-Led Strategy” are the only sustainable moats.

Get Your SEO Strategy