The search engine optimization market in Egypt represents a sector characterized by high operational volume but a significant deficit in strategic “Only-ness.” An analysis of 30 distinct SEO agencies operating across major hubs—including Cairo (Maadi, Nasr City, New Cairo), Giza (Dokki, Sheikh Zayed), Alexandria, Port Said, Mansoura, and the Suez Canal zone—reveals a market that is technically functional but strategically stagnant.

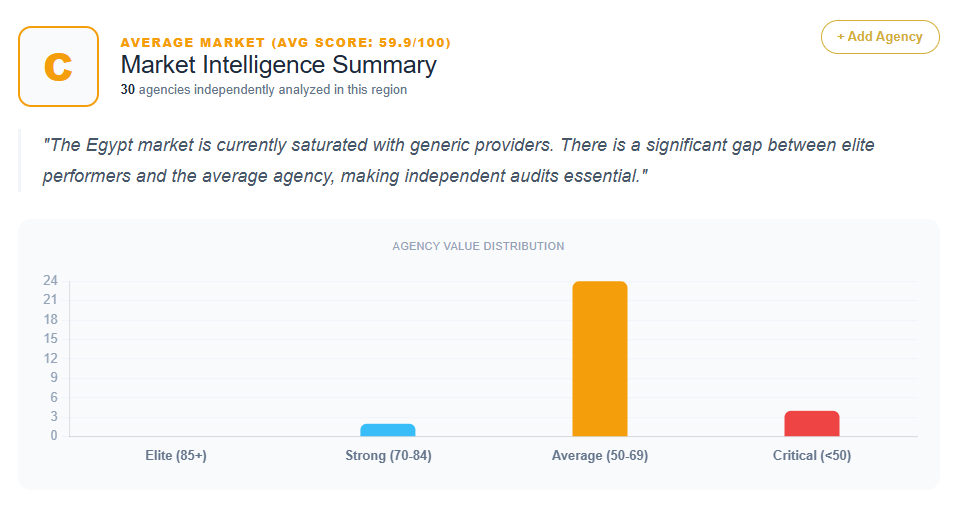

The diagnostic data for these 30 providers shows a performance spectrum that peaks at a score of 78 (Chain Reaction) and floors at 38 (Pioneer Tech). While the technical “floor” of the market is stable, a pervasive theme of “Generalist Dilution” prevents the majority of agencies from achieving elite-tier positioning. For businesses seeking organic growth in Egypt, the challenge lies in distinguishing between “commodity vendors” who list features and “strategic partners” who architect revenue.

The Performance Hierarchy: Analyzing the Scoring Tiers

The quantitative data provides a clear tiered structure of the Egyptian SEO landscape. Only two agencies—Chain Reaction (78) and Growth EG (72)—successfully break into the 70+ “Performance” bracket. These firms are noted for high-tier technical capabilities and modern UI/UX, yet even they are penalized for “Regional Genericization” or “Strategic Ambiguity,” failing to fully bridge the gap between regional scale and the specific nuances of the Egyptian consumer.

The vast majority of the market resides in the “Mid-Tier Sea of Sameness,” with 15 agencies scoring between 62 and 68. This cluster includes firms like Smart Vision, Digitree, G-Dart, BeBrand, and Textile Digital, all of which share a score of 68. This clustering highlights a major market bottleneck: agencies in this tier are professionally presented and locally trusted, but they use interchangeable “full-service” messaging that makes them indistinguishable from one another in a clinical audit.

At the lower end of the spectrum, scoring below 60, are legacy providers and IT-centric firms such as Media Gate (58), Alex Design (58), Pioneers Solutions (58), Suez Ads (58), Techno Masr (58), Delta Soft (58), and Pioneer Tech (38). These firms are consistently diagnosed with an “Identity Crisis,” where SEO is treated as a secondary add-on to hardware solutions, web hosting, or traditional advertising.

The “Generalist Trap” and Strategic Dilution

Perhaps the most significant finding across the 30 diagnoses is the prevalence of “Generalist Dilution.” Agencies like Pioneers Solutions, Target Marketing, and Alex Design bundle high-stakes SEO with low-tier lateral services such as hardware sales, printing, hosting, or giveaway services.

The data suggests that this positioning signals a lack of “Subject Matter Authority” to the market. For instance, Target Marketing (58) is diagnosed as having “Ego-Centric Messaging” that prioritizes what the agency does rather than what the client achieves. Similarly, Digitree Inc. (68) and BeBrand (68) are penalized for purely descriptive messaging (“We offer SEO services”) rather than performance-driven narratives. This dilution creates a “Substitution Test” failure—if the brand name were removed from the site, the value proposition would be identical to a hundred other providers in Cairo.

Geographic Ceilings: Cairo vs. The Provinces

The analysis shows a distinct strategic divide based on location:

- Cairo and Giza (The Competitive Center): Firms in Maadi (G-Dart, BeBrand, Click Media, Textile Digital) and Sheikh Zayed (Digitree, Smart Code) face the highest competition. They are under intense pressure to move from “service lists” to “ROI frameworks.” However, many, like Unplugged (64) and Textile Digital (68), fall into the “Creative Agency Syndrome,” where visual “vibe” and “storytelling” are prioritized over technical search performance.

- Regional Hubs (The Local Specialists): Agencies in Mansoura (Techno Masr, Delta Web), Alexandria (Alex Design, Delta Soft), and the Suez Canal zone (Canal Digital, Suez Digital, Suez Ads) often rely on “Geographic Proximity” as their primary differentiator. The data characterizes this as a “Geographic Crutch,” which inadvertently signals a ceiling on their capabilities, making them invisible to national enterprise clients who prioritize ROI over proximity.

The Missing Moat: Arabic-Language SEO Nuance

A recurring prescription across nearly all 30 agencies is the need to master and market “Arabic-First” search strategies. Despite the unique linguistic requirements of the Egyptian market, agencies like Vocus Digital (62), Media Gate (58), and Ebda3 Digital (54) are warned for not explicitly addressing “Arabic script challenges” and “bilingual search intent.”

The data highlights this as a major untapped differentiator. Agencies that can successfully navigate the transition from traditional to digital-first consumer behavior in Arabic are positioned to escape the “Commodity Trap.” For example, the prescription for Chain Reaction (78) emphasizes a pivot from “Technical Excellence” to “Local Search Intent & Arabic Nuance” to reclaim market share from “Dubai exports.”

Quantifying the ROI of Strategic Misalignment

The financial cost of failing to differentiate is explicitly quantified in the dataset’s ROI notes. The “Genericity Tax” manifests in several ways:

- Conversion Leaks: Agencies like Vocus Digital and Nox Agency are estimated to suffer a 20–30% leak in their lead-to-opportunity conversion rates due to generic globalized messaging.

- Price Sensitivity: When an agency is perceived as a commodity (e.g., Alex Design or Ebda3 Digital), it is forced into “price-based negotiations,” likely resulting in a 30–50% loss in potential annual contract value (ACV).

- Lead Quality: For firms like Suez Digital (42) and Smart Code (42), the lack of a specialized value prop leads to a “high bounce-on-contact” rate from qualified leads, as sophisticated buyers prioritize specialized growth partners over task executors.

The Path Forward: From Services to Systems

To move from the 50s and 60s into the 80+ “Expert” tier, the 30 analyzed agencies are given clear tactical prescriptions. The most consistent advice is the “Productization” of SEO services into named, proprietary frameworks.

The dataset identifies several proposed methodologies to bridge this gap:

- The Vocus Local-to-Global Engine

- The Digitree Search-to-Revenue Framework

- The Essence Optimization Protocol

- The Cairo-Growth Protocol (for Codex Egypt)

- The Canal-7 SEO Sprint

- The Suez-SEO Delta Framework

- The Delta Search Framework

By naming their processes, agencies can move from selling “labor hours” to selling “intellectual property,” which justifies premium pricing and reduces sales friction. Furthermore, agencies are urged to replace generic headlines with “Impact Headlines” that cite specific Egyptian market results—such as “Increasing Organic Revenue for Egyptian E-commerce by 40%” (Ebda3) or “Dominating Egyptian Search Results for High-Growth Brands” (Suez Ads).

Conclusion: The Strategic Evolution of Egyptian SEO

The analysis of 30 providers indicates that the Egyptian SEO market is technically mature but strategically underdeveloped. The industry is home to “Software Houses,” “Creative Boutiques,” and “Integrated Shops,” but very few “Search Powerhouses.”

The data concludes that while the “technical foundation” is solid, the “strategic narrative” is currently missing. Agencies that can successfully decouple from the generalist model, lean into the complexities of Arabic search intent, and productize their methodologies will define the next phase of market leadership in Egypt. Until this shift occurs, the majority of the market will remain trapped in price-sensitive competition, struggling to prove the “So What?” to an increasingly sophisticated and ROI-conscious Egyptian corporate sector.

Get Your SEO Strategy