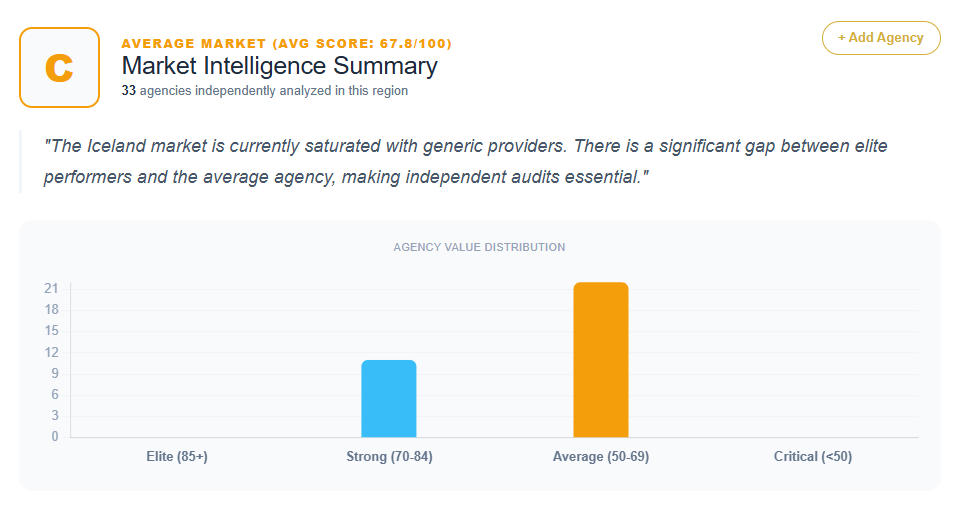

An analysis of 33 distinct SEO agencies and digital service providers currently operating in Iceland reveals a market defined by professional aesthetic standards but a significant deficit in specialized search authority. Centered primarily in the Reykjavík business districts—with notable outposts in Kópavogur, Hafnarfjörður, and Akureyri—the industry is currently grappling with what diagnostic data identifies as “Generalist Dilution.” While technical proficiency is present, only a small fraction of the market has successfully moved from being service vendors to strategic growth partners.

The quantitative data provided indicates a performance spectrum peaking at a score of 78 (Digital.is and Novus) and reaching a low of 58 (Vefsíðugerð.is). The heavy concentration of scores between 62 and 68—representing over 60% of the analyzed group—suggests a “Sea of Sameness” where agencies meet basic operational requirements but fail to articulate a unique strategic reason for high-value enterprise selection.

The Performance Hierarchy: Analyzing the Scoring Tiers

The Icelandic SEO market is sharply tiered based on an agency’s ability to bridge the gap between “aesthetic production” and “clinical search dominance.”

High-Authority Mid-Market (Scores 74–78)

Agencies such as Digital.is (78), Novus (78), Sahara (76), Pipar\TBWA (76), and Marketing.is (74) represent the top tier of authority in the dataset. Sahara and Pipar\TBWA lead on brand recognition and scale, yet both are penalized for “Generalist Dilution,” where their SEO offerings are buried within broad creative suites. Digital.is and Novus achieve higher scores through clearer performance mapping, but even these firms are cautioned against the “Generalist Commodity Trap,” as they rely on broad terms like “vöxtur” (growth) and “árangur” (results) rather than unique, data-driven methodologies.

The Professional Generalist Tier (Scores 68–72)

This segment is the most competitive and includes agencies like Snjall.is (72), Pixel (72), Vefstofan (72), Arkiv (72), Birting (72), and Hlynur.is (72). These agencies are professionally presented but are frequently diagnosed with “Service-Commodity Drift.” For instance, Snjall.is and Vefstofan are noted for focusing on the “what” (SEO, ads, web design) rather than the “why” or the business outcome. This prevents them from ascending to a market-leading status, as they appear as reliable executors rather than unique market disruptors.

Regional and Utility Providers (Scores 58–64)

The lower tier includes regional specialists and technical utility providers such as Hvítahúsið (62), Advania (62), Stefna (62), Vefsetur (62), and Vefsíðugerð.is (58). These firms are consistently diagnosed with an “Identity Crisis.” Advania and Stefna, both significant names in the IT and software sector, treat SEO as a secondary technical add-on or “Leitartækni” (search technology). The data for these firms indicates a brand-perception gap where marketing directors view them as IT vendors rather than growth catalysts.

Recurring Strategic Weaknesses: The Generalist Trap

The most prevalent diagnosis across the 33 providers is “Generalist Dilution.” In the Icelandic market, agencies frequently lead with a “360-degree” or “Full-Service” narrative, which the data suggests is a primary cause of authority dilution.

Creative vs. Technical Misalignment

Agencies such as Hvítahúsið, Arkiv, and Vefmynd (64) prioritize “Creativity that works” (Sköpun sem virkar) or aesthetic “magic.” While visually superior, this creates a “Strategic Misalignment” for clients seeking aggressive organic growth. The data suggests that without a clear performance-centric hook, creative agencies are often perceived as “too artsy” for technical search challenges. For Pipar\TBWA, this results in an estimated 15-22% “Specialist Leak” to more focused technical competitors.

The Utility and Maintenance Perception

Firms like Vefsetur, Vefumsjón (62), and Vefsíða.is (62) bundle SEO with infrastructure services like WordPress maintenance and hosting. The diagnostic data for Vefumsjón notes that by framing SEO as a “technical chore” (security updates, speed optimization), they invite price-based comparisons rather than value-based partnerships. This “Utility Trap” prevents the acquisition of high-margin, long-term retainers, as clients view the service as an expense to be minimized.

Geographic Patterns: The Nerve Centers of Icelandic Search

The physical location of an agency in Iceland significantly correlates with its strategic flaws:

- Reykjavík (The Nervecell): Concentrated in districts like Katrínartún, Guðrúnartún, and Borgartún. Agencies here, such as Sahara and Hvítahúsið, compete on “Institutional Credibility” but often pay a “Genericism Tax,” as prospects view their messaging as interchangeable. The Laugavegur 178 address houses a cluster of providers (Pixel, Tengill, Concept, Arkiv), contributing to a lack of differentiation in a saturated metro market.

- Kópavogur (The Boutique Hub): Hub for Kársnes (62), Markaðsdeildin (68), Vefsetur (62), Hlynur.is (72), Novus (78), Vefgerð (68), Vefari (68), and Upplifun (62). These firms often have high local trust but suffer from “Strategic Anemia.” Markaðsdeildin, for instance, is noted for its “outsourced department” model, which prioritizes convenience over the specialized technical depth required for enterprise-level SEO.

- Akureyri (The Northern Outposts): Agencies like Kodi (68) and Stefna (62) represent the northern market. Kodi is noted for being a creative powerhouse in Akureyri, but its SEO specialization remains secondary to design, leading to lower lead-to-close ratios for high-ticket recurring contracts.

Local Market Nuances: Linguistic Authority and Niche Dominance

The Icelandic digital economy possesses unique cultural and linguistic drivers that many agencies fail to leverage. A recurring theme in the prescriptions for firms like Digital.is, Snjall.is, and Pixel is the failure to explicitly market “Icelandic Search Authority.”

The data identifies “Search Intent Dominance” as a major untapped differentiator. Agencies that treat search intent as a “one-size-fits-all” model are losing ground to firms that can demonstrate mastery of the local linguistic landscape. For example, the prescription for Pixel (72) suggests a “Performance Bridge” that links technical web development directly to quantifiable organic traffic gains in the .is TLD space.

Quantifying the ROI of Strategic Misalignment

The financial consequences of poor differentiation are explicitly quantified in the dataset’s ROI notes for these 33 providers:

- Lower Lead-to-Close Ratios: Generic messaging for firms like Sahara and Tengill results in projected 15-20% lower conversion rates on specialized SEO inquiries.

- Conversion Leakage: Agencies that do not quantify their impact through revenue-first messaging (e.g., Markaðsdeildin, Vefgerð) experience an estimated 20-30% leakage in potential lead conversion.

- The “Commodity Tax”: For mid-tier firms like Digital.is and Novus, the lack of a sharp “Only-at-Digital.is” hook results in a 15-25% “genericism tax” where prospects prioritize hourly rates over business-case ROI.

- Price-Sensitivity Friction: Agencies like Kársnes and Vaki are forced into “Price-Sensitivity Traps,” leading to higher client churn and an inability to justify premium “Specialist” pricing.

Strategic Prescriptions for Market Dominance

Across the 33 agencies, the recommendations for growth center on a single movement: the transition from “what we do” to “the financial delta we create.” To dominate the Icelandic market, agencies are urged to:

- Move to “Outcome-First” Logic: Transition headlines from service descriptions to quantifiable revenue claims. Examples include “Dominating Icelandic Search to Drive Your Bottom Line” (for Sahara) or “Increasing Organic Revenue by 150%” (for Kodi).

- Pivot to “Search Share” Narrative: Replace generic growth promises with a focus on “Organic Market Share” and “Revenue Attribution.” This is a critical recommendation for Birtingahúsið and Hvítahúsið.

- Isolate SEO as a Strategic Pillar: Decouple performance marketing from creative production (for firms like Sahara and Pipar\TBWA) or IT maintenance (for Advania and Stefna) to build specialized authority.

- Vertical Specialization: Instead of “Digital Agency,” firms are advised to become the authority for specific sectors like Tourism, Fisheries, or specialized local E-commerce to escape the generalist trap.

Conclusion: Strategic Outlook

The Iceland SEO market is technically mature but strategically quiet. The industry is currently divided between “Creative Powerhouses” that are too broad and “Technical IT Shops” that are too literal.

The data concludes that technical proficiency is no longer a differentiator in Reykjavík; it is a baseline expectation. The agencies that will dominate the next decade are those that can successfully decouple their marketing from generic jargon and lead with revenue-centric narratives. Until the mid-tier agencies in Kópavogur and the metro center stop listing services and start architecting market dominance, they will continue to pay the “Genericity Tax” through compressed margins and higher client churn. The path forward lies in owning the “Search Intelligence” niche and proving clinical ROI in a small, high-competition economy.

Get Your SEO Strategy