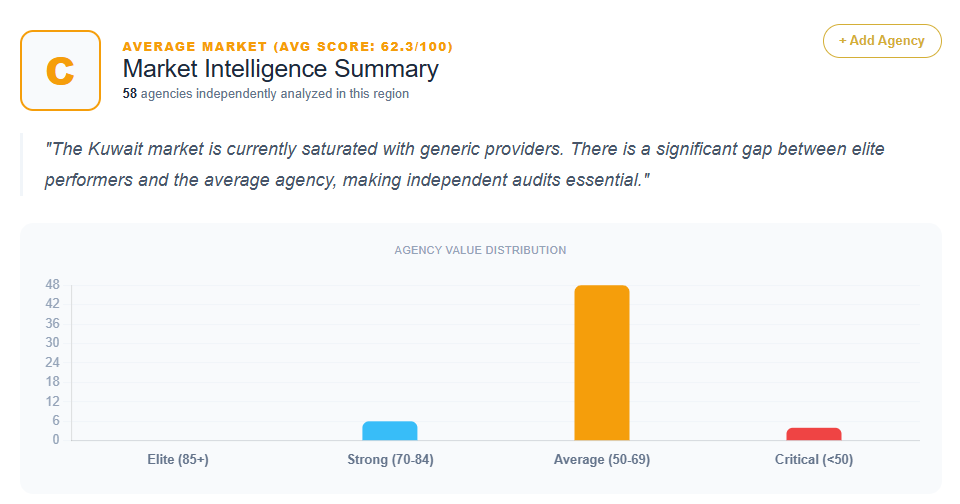

An analysis of the search engine optimization market in Kuwait, based on diagnostic data from 58 distinct agencies and consultants, reveals a landscape defined by high local trust and technical competency, yet a significant deficit in strategic differentiation. Concentrated primarily in the business hubs of Kuwait City—specifically in Sharq, the Al Hamra Business Tower, and the Al-Soor Street corridor—the industry is currently struggling to move beyond commodity-level service delivery toward performance-led growth engineering.

The quantitative data provided shows a performance spectrum peaking at a score of 74 (The 7 Group, Yellow Submarine) and reaching as low as 42 (Pioneers for Computer Systems, Static Leaf). The heavy concentration of scores between 58 and 68—representing over 70% of the analyzed group—suggests a “Sea of Sameness” where agencies meet basic operational requirements but fail to provide a unique strategic reason for high-value enterprise selection. In a market where high-net-worth sectors like Finance, Oil & Gas, and Luxury Retail dominate, the gap between “standard vendors” and “strategic partners” is the primary barrier to market leadership.

The Performance Hierarchy: Analyzing the Scoring Clusters

The Kuwaiti SEO market is tiered based on an agency’s ability to bridge the gap between technical optimization and commercial ROI.

High-Authority Strategic Performers (Scores 70–74)

A small group of agencies, including The 7 Group (74), Yellow Submarine (74), DSRPT (72), Tocaan (72), Raybal Group (72), and Expanda (72), represent the top tier of authority in this dataset. These firms are distinguished by their high brand equity and modern UI/UX. However, even these leaders face significant strategic hurdles. For instance, Yellow Submarine is diagnosed with the “Creative Agency Trap,” where messaging prioritizes aesthetics over the performance-driven search results required for organic dominance. DSRPT, while technically sound, is cautioned for “Geographic Dissonance,” as its brand voice feels like a “global export” that fails to address the specific bilingual search complexities of the Kuwaiti market.

The Mid-Market “68 Club” (Score 68)

A significant concentration of providers—including Mawaqaa, Target Interactive, Ice Tulip, Chrisans Digital, Bowaba, Easy Devs, Chrisans Group, Waves Media, M2R Group, and Sine Marketing—all share the score of 68. This clustering highlights a major market bottleneck: these agencies are professionally presented and locally trusted, but they use interchangeable “full-service” messaging. Bowaba, for instance, is noted for “Generalist Dilution,” where its status as a creative shop undermines its perceived authority as a technical SEO specialist in a market that increasingly demands data-centric ROI.

The Commodity and Generalist Tier (Scores 42–64)

The largest segment of the market scores 64 or below. This includes firms like Design Master (64), KuwaitNET (62), Logic Media (58), Nervio Tech (58), Carlita Tech (48), CliqTechno (54), and Kuwait Digital Marketing (45). These providers are consistently diagnosed with “Strategic Anemia” or “Generalist Dilution.” In many cases, SEO is marketed as a secondary technical add-on to unrelated services like ERP systems, hosting, or legacy IT infrastructure.

Recurring Strategic Weaknesses: The Generalist Trap

The most prevalent diagnosis across the 58 providers is “Generalist Dilution.” In the Kuwaiti market, agencies frequently lead with a “360-degree” or “Full-Service” narrative, which the data identifies as a primary cause of authority dilution.

IT and Software-House Myopia

Firms such as KuwaitNET (62), iTechnology Solutions (62), Merak Technologies (64), and Nervio Tech (58) lead with their IT infrastructure or software development roots. The diagnostic data suggests this makes their SEO offering feel like a “supplemental utility” rather than a primary growth engine. For Pioneers for Computer Systems (42), the branding is so heavily focused on accounting software that search services are viewed as a peripheral task, leading to a projected 35–50% loss in potential SEO-specific revenue.

Creative vs. Technical Misalignment

Agencies like Sociave (62), Pixel Digital (62), V-Line Media (58), and Pencilvent (64) prioritize aesthetic “creativity” and “vibe.” While visually superior, this creates friction for high-intent SEO leads. The data suggests that without a clear performance-centric hook, creative agencies are often perceived as “design-first,” ceding technical SEO contracts to specialized boutiques. For Sociave, the lack of a data-first pillar results in being relegated to “support” budgets rather than “growth” budgets, costing an estimated 35% in potential high-ticket recurring revenue.

Local Market Nuances: The Bilingual Search Gap

A unique characteristic of the Kuwaiti SEO landscape is the dominance of bilingual (Arabic/English) search behavior. A recurring theme in the prescriptions for firms like DSRPT (72), By Shami (62), Skyhit Media (62), and Adcreators (64) is the failure to explicitly address this complexity.

The data identifies “Bilingual Search Dominance” as a major untapped differentiator. Agencies that treat the market as a global template (e.g., AAMAX (64) or Static Leaf (42)) are losing ground to firms that can demonstrate mastery of the local Kuwaiti Arabic dialect and GCC-specific search intent. For instance, CrackWits (62) is noted for a “Generalist Discount,” as its offshore template messaging fails to capture the prestige and local authority required by sophisticated Kuwaiti enterprises.

Geographic Patterns: Hub Specificity and Trust

The physical location of an agency in Kuwait significantly influences its competitive positioning and trust signals:

- Sharq (The Financial Center): Home to Mawaqaa, Yellow Submarine, Pixel Digital, and others. Agencies here compete on “Institutional Trust” but often pay a “Doubt Tax,” as potential clients spend more time comparing prices because the value proposition isn’t uniquely articulated.

- Al Hamra Tower & Burj Al-Shaya: Hub for Target Interactive, iGroup, Waves Media, and Carlita Tech. These addresses signal “Corporate Stability,” but the data warns that global brand names like International Group (62) often rely on prestige as a surrogate for actual technical search strategy.

- Salmiya & Hawalli (The Regional Challengers): Agencies like DSRPT, Dary Web, and Branding Mart represent this segment. They are cautioned that a lack of industry-specific “Authority Signals” in their messaging makes them indistinguishable from lower-cost freelancers.

Quantifying the ROI of Strategic Misalignment

The financial consequences of poor differentiation are explicitly quantified in the dataset’s ROI notes for these 58 providers:

- Lead-to-Close Leakage: Generic positioning for agencies like Tocaan (72) and Chrisans Group (68) result in projected 20–30% lower conversion rates on specialized SEO inquiries.

- Conversion Leaks: Agencies that do not quantify their impact through revenue-first messaging (e.g., Going Up Digital (62)) experience an estimated 15–25% leakage in potential conversions.

- The “Commodity Trap”: For mid-tier firms like Softline Solutions (62) and Artek Agency (64), the lack of a sharp differentiator results in a 25–35% lower lead quality score and forces competition on price rather than value.

- Specialist Premium Loss: Creative boutiques such as Born or Yellow Submarine are noted to potentially leave 20–30% of potential revenue on the table because they fail to lead with search performance metrics.

Prescriptions for Market Dominance: The Shift to Outcomes

Across the 58 agencies, the recommendations for growth center on a single movement: the transition from “what we do” to “the financial outcomes we generate.” To lead the Kuwaiti market, agencies are urged to:

- Move to “Revenue-First” Logic: Transition headlines from service descriptions to quantifiable revenue claims. The data suggests replacing lists of “SEO Services” with narratives like “Dominating Kuwaiti search landscapes” or “Revenue-driven search strategy.”

- Segment Brand Messaging: Firms with IT or software roots (e.g., Sada Al-Afkar and iTechnology Solutions) are encouraged to decouple digital growth from general IT support to build specialized search authority.

- Vertical Specialization: Instead of “General Digital Marketing,” agencies are encouraged to become the authority for specific sectors like Luxury Retail, Real Estate, Oil & Gas, or Financial Services.

- Localized Trust Signals: The market demands proof of concept in local KWD (Kuwaiti Dinar) growth metrics and Arabic search intent. Agencies that fail to highlight these regional factors remain “strategically invisible.”

Conclusion

The Kuwait SEO market is technically sound and geographically well-entrenched but strategically stagnant. The industry is currently divided between “Creative Boutiques” that are too aesthetic, “IT Integrators” that are too technical, and “Legacy Generalists” that are too broad.

The data concludes that technical proficiency is no longer a differentiator in Kuwait City; it is the “Floor.” The agencies that will dominate the next decade are those that can successfully productize their expertise and pivot their messaging from “Online Presence” to “Market Share Acquisition.” Until the mid-tier agencies stop listing services and start architecting revenue, they will continue to pay the “Genericity Tax” through lower margins and high client churn. The path to leadership lies in owning the “Bilingual Authority” niche and proving clinical ROI in a market that values precision above all else.

Get Your SEO Strategy