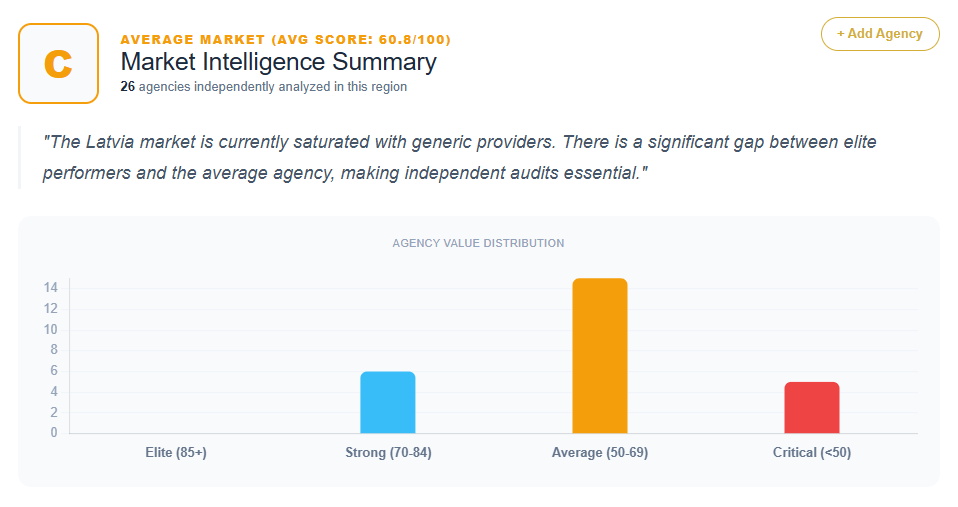

An analysis of 26 SEO agencies and digital service providers currently operating in Latvia reveals a market characterized by professional technical execution but a significant deficit in strategic differentiation. Centered primarily in the Riga business hub—with additional regional presence in Ventspils, Mārupe, and Ogre—the industry is currently struggling with what diagnostic data identifies as the “Commodity Trap.” While the technical floor of the market is stable, only a fraction of providers have successfully moved from being service vendors to strategic growth partners.

The quantitative data provided indicates a broad performance spectrum. Agency scores peak at 84 (iMarketings.lv) and reach a low of 32 (Ogrenet). A heavy concentration of scores resides between 58 and 68, representing over 50% of the analyzed group. This clustering suggests a market saturated with “Safe Generalists”—firms that are technically competent but strategically quiet, leading to significant revenue leakage and high price sensitivity.

The Performance Hierarchy: Analyzing the Scoring Tiers

The Latvian SEO market is sharply tiered based on an agency’s ability to bridge the gap between “technical optimization” and “financial ROI.”

High-Authority Performers (Scores 74–84)

Only a small group of agencies, including iMarketings.lv (84), Top Media (78), and SEM (74), represent the top tier of authority in Latvia. These firms distinguish themselves through Google Premier Partner status and institutional credibility. However, even at this level, the data notes a “Strategic Anonymity” or “Corporate Genericism.” For example, SEM is penalized because its messaging is indistinguishable from other top-tier Baltic agencies, focusing on “channel execution” rather than “business outcomes.”

Mid-Market Contenders (Scores 62–72)

This segment is the most competitive and includes agencies like Bright (72), IMEDIA (72), Infinitum Agency (72), DigiTrade (68), and Finnov Studio (68). These agencies are professionally presented but are frequently diagnosed with “Strategic Stagnation.” The diagnosis for Infinitum highlights that terms like “data-driven” and “result-oriented” have transitioned from differentiators to baseline expectations in the Latvian market. This leads to what the data calls “Performance Parity,” where potential clients struggle to distinguish one high-end firm from another.

Regional and Low-Tier Providers (Scores 32–58)

The lower tier includes regional generalists and legacy IT providers such as DEX (58), SEO Audits (58), Digitālais Centrs (58), SIA SoftServiss (38), and Ogrenet (32). These firms are consistently diagnosed with “Generalist Dilution.” In many cases, SEO is marketed as a secondary technical “add-on” to unrelated services like hardware maintenance, computer repair, or internet utility provision.

Recurring Strategic Weaknesses: The Generalist Trap

The most prevalent diagnosis across the 26 providers is the “Generalist Trap.” In the Latvian market, agencies frequently lead with a “360-degree” or “Full-Service” narrative, which the data suggests is a primary cause of authority dilution.

IT Utility vs. Strategic Growth

Firms such as SIA SoftServiss and IT Serviss (42) bundle SEO with legacy IT services. The diagnostic data for SoftServiss notes that a “repair shop” perception triggers a price-floor trap, where the agency can only compete on low costs. Similarly, Ogrenet is noted for a “fatal dilution” of its value proposition because its primary identity is as an Internet Service Provider (ISP), causing SEO to appear as a legacy technical commodity rather than a growth lever.

Creative vs. Technical Misalignment

Agencies like Bright (72) prioritize aesthetics and UX/UI under the slogan “Digital products with character.” While visually superior, this creates a “Strategic Misalignment” for clients seeking aggressive organic growth. The data suggests that without a clear performance-centric hook, creative agencies are often perceived as a “high-cost design choice” rather than a revenue-generating partner, potentially costing them 20–30% in missed retainer opportunities.

Local Market Nuances: The Localization Failure

The dataset includes specific findings on how agencies navigate (or fail to navigate) the unique complexities of the Latvian search environment.

Bilingual Search Complexity (LV/RU)

A recurring theme in the prescriptions for firms like SEO Audits (58), IdeaTurf (42), and Finnov Studio (68) is the failure to explicitly address the Latvian/Russian bilingual search landscape. The data identifies this trilingual complexity (Latvian, Russian, and English) as a major untapped differentiator. Agencies that treat search intent as a “one-size-fits-all” model are losing ground to firms that can demonstrate mastery of these regional linguistic nuances.

The Trust Gap with Offshore Providers

IdeaTurf (42) represents the risk of non-localized offshore models. Based in Bangladesh, the agency competes on price but lacks native language capabilities and local trust signals. The data predicts a 65–75% drop-off in the conversion funnel for such providers because Latvian B2B clients prioritize physical proximity and regional contextual relevance.

Quantifying the ROI of Strategic Misalignment

The financial consequences of poor differentiation are explicitly quantified in the dataset’s ROI notes for these 25 providers:

- Conversion Leakage: Generic positioning for agencies like E-Aģentūra (58) and DigitalMore (64) results in a projected 20–30% loss in potential high-ticket conversions.

- Sales Cycle Inflation: For high-authority firms like Infinitum (72) and SEM (74), the lack of a “Strategic Hook” leads to sales cycles being 15–20% longer as prospects view the service as a premium commodity rather than a unique ROI-multiplier.

- Price Sensitivity: Agencies like DEX (58) and Sellprom (62) are forced into “Price-Based Competition.” This “race to the bottom” results in lower lead-to-close ratios because prospects view the service as a cost center to be minimized rather than an investment to be scaled.

- Trust Deficit: Offshore or non-localized entities like IdeaTurf face a “Relevance Bounce Rate,” where the cost of acquisition for regional leads remains unsustainably high.

Patterns in Value Propositions: Descriptive vs. Outcome-Driven

The majority of Latvian agencies rely on “Descriptive Functionalism.” This is evident in the messaging of firms like Apinis SEO (62) and 79.lv (58), which focus on SEO tasks—audits, keywords, and links—rather than business outcomes.

The data identifies a recurring “Commodity Loop” in the Riga hub. For instance, DigiTrade (68) is noted for “Strategic Anonymity,” where its service descriptions are interchangeable with dozens of other agencies. Even agencies with strong category-relevant domains, such as E-komercija.lv (64), fall into the “service-catalog” trap, offering generic promises of “increased sales” that fail to justify premium pricing for high-ticket enterprise clients.

Prescriptions for Market Dominance: The Shift to Outcomes

Across the 26 agencies, the prescriptions for growth center on a single movement: the transition from “what we do” to “how much the client earns.” To dominate the Latvian market, agencies are urged to:

- Move to “Economic Outcomes”: Shift headlines from “SEO Services” to “Market Share Growth” or “Revenue-Driven Search Strategy.”

- Segment by Business Stage: Address specific pain points like “SEO for International Export” (for iMarketings.lv) or “SME Local Dominance” (for DigiTrade).

- Inject Quantitative Proof: Move from generic “results-oriented” claims to hard data, such as “Average 40% organic growth for LV retail.”

Conclusion: The Path Forward

The Latvia SEO market is technically mature but strategically underdeveloped. The industry is currently divided between “Full-Service Giants” who are too broad and “IT Generalists” who are too technical.

The data concludes that technical proficiency is no longer a differentiator in Latvia; it is a baseline expectation. The agencies that will define the next phase of market leadership are those that can successfully decouple their marketing from generic jargon and lead with revenue-centric narratives. Until the middle-tier agencies in Riga and regional hubs stop listing services and start architecting market share, they will continue to pay a “Genericity Tax” through compressed margins and extended sales cycles. The only sustainable moat in the saturated Baltic landscape is a clear, outcome-focused strategic narrative.

Get Your SEO Strategy