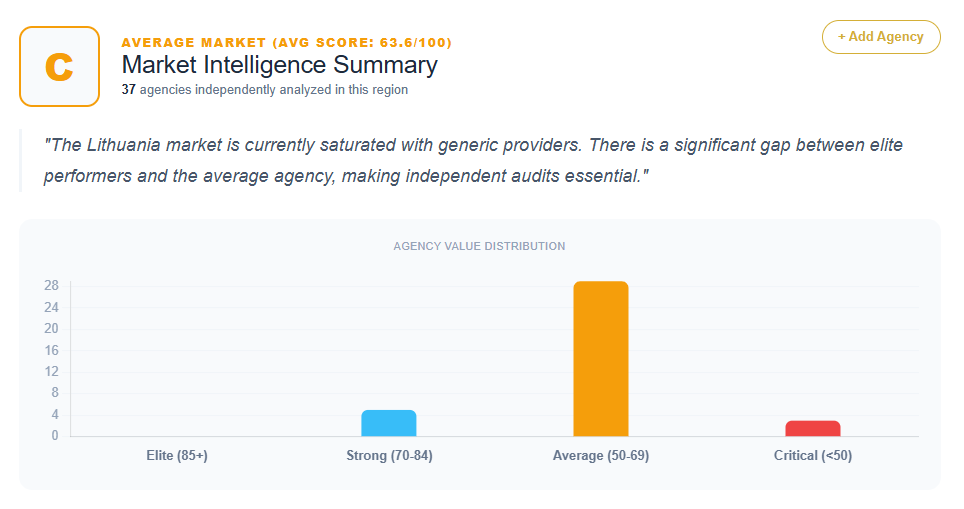

An exhaustive analysis of 37 SEO agencies and consultants operating within the Lithuanian digital ecosystem reveals a market defined by high technical competence but a significant deficit in strategic “Only-ness.” While the technical floor of the industry is solid, the diagnostic data suggests that a vast majority of providers struggle with what is frequently identified as “Generalist Dilution” or “Strategic Anemia.”

The performance scores in this dataset range from a market high of 82 (Good One) to a low of 34 (Infomaze Technologies). The quantitative data shows a heavy concentration of agencies scoring between 62 and 68—representing nearly 50% of the analyzed group. This clustering highlights a “Sea of Sameness” in the Baltic region, where agencies meet basic operational requirements but fail to provide a unique strategic reason for high-value enterprise selection.

The Performance Hierarchy: Analyzing the Scoring Tiers

The Lithuanian SEO market is tiered by its ability to bridge the gap between “technical tasks” and “business outcomes.”

The Authority Tier (Scores 76–82)

Only a handful of agencies achieve elite status. Good One (82) leads the market, leveraging its status as a Google Premier Partner and institutional trust with brands like Telia and IKEA. However, even this leader is diagnosed with “Strategic Misalignment,” as its narrative is rooted in legacy rather than a unique, proprietary methodology. Pionieriai (78) and Zest (76) follow closely, utilizing strong metaphors and modern UX. However, Pionieriai is noted for “Strategic Abstraction,” where creative positioning occasionally masks specific technical ROI evidence.

The Mid-Market Performance Tier (Scores 64–72)

This is the most crowded segment, containing agencies like Whatabout (72), SEO mama (72), and a cluster of firms at the 68 mark, including MarketRats, SEO Helis, Addicted, APG Media, Fresh Media, Webpro, and Reklamos projektai. These agencies are professionally stable but often suffer from “Commoditized Excellence.” For instance, SEO Helis is penalized for leading with the cliché that “SEO is an investment,” which fails to establish a unique competitive advantage. SEO mama possesses high niche recognition but is cautioned that its “maternal positioning” risks appearing less scalable to clinical, data-first enterprise clients.

The Generalist and Regional Tier (Scores 34–62)

The lower end of the spectrum features regional providers and international entities with poor localization. Agencies like Verslo angelas (52), Aitvaras (62), and Webas (62) are frequently diagnosed with “Generalist Dilution,” where SEO is offered as one of many ingredients in a “commodity catalog.” The bottom tier includes firms like UAB Utenos reklama (42) and Jonavos reklama (42), where search services are bundled with physical production such as car wrapping, engraving, and billboards, severely diluting their perceived digital authority.

Recurring Strategic Weaknesses: The Generalist Trap

The most prevalent diagnosis across the 37 agencies is “Generalist Dilution.” In the Lithuanian market, many firms attempt to be a “one-stop-shop” for all IT and marketing needs, which the data suggests is a major bottleneck for high-ticket acquisition.

IT and Infrastructure Dilution

Firms like Creative Partner (68), IT Pasaulis (58), and ITpaslaugos.lt (54) lead with their technical development roots. While they possess superior technical foundations, they treat SEO as a “bolt-on” or “auxiliary” service. The diagnosis for Creative Partner notes that this creates friction for clients seeking high-level organic growth, as the site appears to be a “dev shop that also does marketing.” Similarly, ITpaslaugos.lt is cautioned that grouping SEO strategy with hardware maintenance dilutes their authority as strategic growth partners.

Creative vs. Technical Misalignment

Agencies such as Whatabout (72) and Addicted (68) prioritize aesthetics and “sincere marketing” over data-driven language. The data indicates this leads to “Comparison Friction,” where potential high-value leads perceive these firms as creative studios rather than technical performance powerhouses. Addicted’s reliance on “sincerity” as a primary differentiator results in a longer sales cycle, as trust must be built manually rather than through a pre-validated strategic framework.

Geographic Patterns: Vilnius Hub vs. The Provinces

The physical location of an agency in Lithuania significantly influences its competitive positioning and strategic flaws:

- Vilnius (The Competitive Epicenter): Home to Good One, Zest, and Pionieriai. Agencies here compete on “Institutional Credibility” but often pay a “Commodity Tax,” as prospects view them as interchangeable. MarketRats (68) and Progressus Digital (68) represent the Vilnius mid-market, characterized by “Safe Messaging” that fails to disrupt the mental shelf-space of high-value prospects.

- Kaunas (The Technical Secondary Hub): Hub for Raibec (68), Webpro (68), and Webas (62). These firms often have high technical competence but suffer from “Strategic Safety.” Raibec is noted for its technical transparency but is criticized for failing to establish a “Growth Partner” narrative that separates it from standard service providers.

- Regional Hubs (Utena, Jonava): Agencies in smaller regions are heavily penalized for “Generalist Dilution.” The diagnosis for Utenos reklama (42) highlights the friction of grouping SEO with traditional physical labor, which signals a lack of strategic depth to sophisticated B2B clients.

Local Market Nuances: The Localization Failure

The dataset includes a critical outlier: Infomaze Technologies (34). This agency is identified as having “zero localization” for the Lithuanian market. It fails to acknowledge linguistic, cultural, or technical nuances such as Lithuanian morphology or localized SERP features. The diagnostic data suggests that businesses using such generalist offshore providers risk a 50% loss in potential conversion value by failing to address local search intent correctly.

Quantifying the ROI of Strategic Misalignment

The financial consequences of poor differentiation are explicitly quantified in the dataset’s ROI notes for these 37 providers:

- Lead-to-Close Leakage: Generic positioning at firms like Zest and Idea Link (64) likely results in a 15-20% lower lead-to-close ratio.

- Revenue Opportunity Gaps: MarketRats (68) is estimated to face a 15-25% lower average retainer value because prospects view the service as interchangeable.

- Pricing Power Erosion: Agencies like IT Pasaulis (58) and Verslo reklama (62) face a “Price-Comparison Trap,” leading to higher client churn and an estimated 25-40% lower Average Contract Value (ACV).

- Sales Cycle Inflation: For firms like Addicted and APG Media, the lack of a “Strategic Hook” forces the sales team to work harder to manually explain differentiation, significantly increasing the cost of acquisition per high-value contract.

Prescriptions for Market Dominance: The Move to Productization

Across the 37 agencies, the prescriptions for growth are remarkably consistent. To move from the 60s into the 80+ “Expert” tier, Lithuanian providers are urged to rename and codify their internal processes. The dataset identifies several specific proposed proprietary frameworks:

- The RATS Growth Protocol (for MarketRats)

- The Helis Velocity Framework (for SEO Helis)

- The Good One Performance Loop (for Good One)

- The StarPath SEO Audit (for Digital Star)

- The Raibec 360 Growth Map (for Raibec)

- The Addiction Growth Model (for Addicted)

- The Angel-Eye Growth Audit (for Verslo angelas)

- The StarPath SEO Audit (for Digital Star)

By shifting from selling “SEO services” (a commodity) to selling a “proprietary mechanism,” agencies move away from hourly-rate perception and justify premium pricing. Furthermore, the data recommends replacing generic headers with “Outcome-First Headlines” that focus on “Market Share Capture” rather than just “Rankings.”

Conclusion: Strategic Outlook

The Lithuania SEO market is currently home to many “safe” agencies and very few “disruptors.” With only one agency scoring above 80, the majority of the Vilnius and Kaunas market remains trapped in price-sensitive competition.

The data concludes that technical proficiency is no longer a differentiator in Lithuania; it is a baseline expectation. The agencies that will dominate the top 5% of the market are those that can successfully productize their expertise and pivot their messaging from “Service Delivery” to “Revenue Optimization.” Until the mid-tier agencies stop listing services and start owning unique methodologies, they will continue to pay the “Genericness Tax” through lower margins and high client churn. The path forward for Lithuanian agencies lies in decoupling from the “Jack-of-all-trades” identity and owning a unique, result-driven “recipe” for growth.

Get Your SEO Strategy