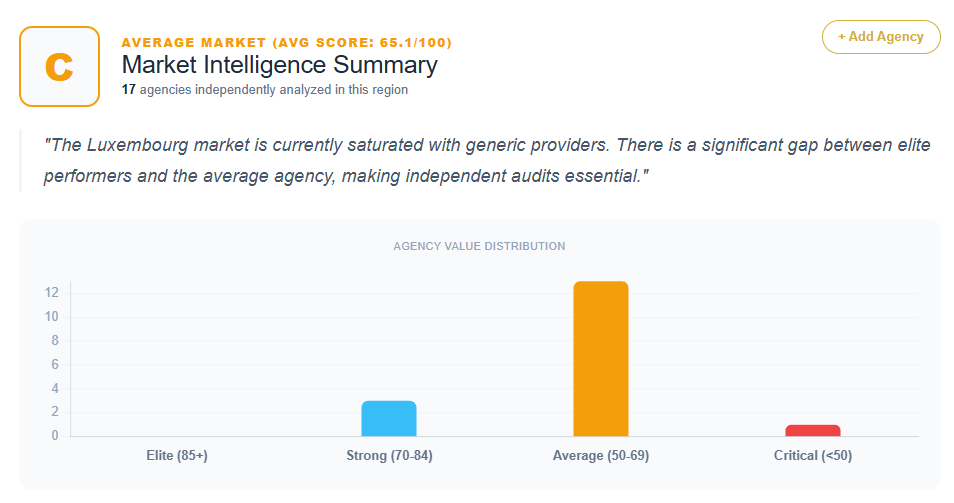

An analysis of 17 distinct SEO agencies and digital consultancies headquartered in Luxembourg—specifically concentrated in hubs like Bertrange, Windhof, Strassen, and the capital city—reveals a market defined by high creative standards but a significant deficit in specialized search authority. Based on diagnostic data, the industry is currently characterized by a struggle to decouple search performance from broad creative branding. While many providers are elite in communication and design, they frequently fail to articulate the technical rigor and data-driven ROI required to dominate high-intent organic search.

The quantitative data provided indicates a performance spectrum peaking at a score of 82 (Vanksen) and reaching a low of 48 (Bunker Palace). A heavy concentration of scores resides between 62 and 68, representing over 50% of the analyzed group. This clustering suggests a market saturated with “Safe Generalists”—firms that are technically competent in digital strategy but “strategically quiet” in the specialized SEO vertical, leading to significant revenue leakage and high acquisition costs.

The Performance Hierarchy: Analyzing the Scoring Tiers

The Luxembourgish SEO market is sharply tiered based on an agency’s ability to bridge the gap between “creative storytelling” and “clinical search dominance.”

High-Authority Consultancies (Scores 72–82)

The top tier is led by Vanksen (82), a premium digital consultancy that wins on institutional scale. However, even at this level, the agency is diagnosed with “Generalist Dilution,” as its SEO offering is often bundled within a broader creative suite, potentially over-complicating the proposition for clients seeking pure organic growth. Nvision (72) and 101 Digital Agency (72) follow, characterized by high technical competence. Yet, both are penalized for a lack of distinct, aggressive SEO value propositions. Nvision is noted for prioritizing “human-centric digital experiences” over measurable search performance, while 101 Digital treats SEO as a secondary “feature” rather than a primary growth engine.

The Creative-Led Middle Tier (Scores 62–68)

This is the most crowded segment, including Noosphere (68), Comed (68), H2A (68), Shine a Light (68), Wili (65), VOUS Agency (64), Strategy (64), and Mikado Publicis (64). These agencies are professionally stable and reputable but frequently suffer from “Strategic Misalignment.” For example, Noosphere’s messaging focuses on “magic” and “stories,” which the data identifies as a friction point for ROI-focused CMOs. Similarly, Comed and Mikado Publicis—legacy players with high brand prestige—position SEO as a modular performance tactic rather than a core strategic driver.

The Low-Authority and Tactical Tier (Scores 48–54)

The lower tier includes regional providers such as W.A.I.T. (54) and Bunker Palace (48). These firms are consistently diagnosed with an “Identity Crisis.” W.A.I.T. suffers from cannibalized authority because it markets IT support, web development, and training simultaneously. Bunker Palace is penalized for a “Creative Bias,” offering zero evidence of data-driven frameworks or search-intent mapping, which renders them “SEO-lite” in the eyes of sophisticated financial and B2B clients.

Recurring Strategic Weaknesses: The Generalist Trap

The most prevalent diagnosis across the 17 providers is “Generalist Dilution.” In the Luxembourgish market, agencies frequently lead with a “360-degree” or “Full-Service” narrative.

Creative Bias vs. Technical Mastery

Firms such as Lola Strategy & Design (62), Wili (65), and Noosphere (68) prioritize aesthetic “meaning” and “production” over technical search audits. The diagnostic data suggests that this “Aesthetic Overload” fails to satisfy the analytical requirements of modern SEO. For Lola, the lack of a performance-centric narrative likely results in a 30-40% loss in potential lead conversion for high-budget transformation projects. Wili is cautioned that treating SEO as a “technical checkbox” prevents them from being perceived as strategic business drivers.

Legacy Inertia and Dated UI/UX

A unique finding in the dataset is the “Visual Trust Deficit” found in legacy utility firms. W.A.I.T. (54) is specifically noted for having a significantly dated website UI/UX, which contradicts their claim of being “web experts.” The data suggests that for such agencies, the brand narrative is a significant liability that prevents them from capturing high-value market share despite having a physical presence in hubs like Dudelange.

Local Market Nuances: The Multilingual SEO Moat

Luxembourg is a unique trilingual search environment (French, German, Luxembourgish, and English), yet the data shows that many agencies fail to leverage “Multilingual Search Strategy” as a core differentiator.

Agencies such as Explose (62), e-connect (64), and Shine a Light (68) are specifically urged to elevate multilingual optimization from a secondary service to a primary regional USP. The data identifies that global agencies often miss these nuances, and local firms that fail to explicitly highlight their ability to navigate the complex FR/DE/LU/EN search landscape lose ground to niche specialists. Explose, for instance, is noted for losing ground to technical boutiques because its messaging lacks the data-centric authority required by the local financial and B2B sectors.

Quantifying the ROI of Strategic Misalignment

The financial consequences of failing to differentiate are explicitly quantified in the dataset’s ROI notes for these 17 providers:

- Lower Lead-to-Close Ratios: Generic positioning for agencies like Vanksen and Nvision results in a projected 15-20% lower conversion rate on high-intent “SEO-only” inquiries.

- “Generalist Discount”: For firms like VOUS Agency and H2A, the lack of a sharp SEO hook forces potential clients to perceive them as “expensive creative choices” rather than “lean ROI generators,” leading to longer sales cycles and lost opportunities for high-margin performance marketing contracts.

- Lead Leakage: Strategy.lu (64) is estimated to suffer a 20-30% loss in high-intent lead conversion because search visibility ROI is not quantified at the first touchpoint.

- Market Share Opportunity Cost: By positioning SEO as an “integrated add-on” (e.g., e-connect), agencies compete on “price and relationship” rather than “measurable financial outcomes,” capping their ability to command premium fees.

Prescriptions for Market Dominance: Shifting to Performance

To move from the 60s into the 80+ “Elite” tier, the 17 analyzed agencies are given clear tactical prescriptions. The most consistent advice involves a radical decoupling of SEO from general digital marketing services:

- Isolate Search Intelligence: Agencies like Vanksen and Comed are advised to architect dedicated landing pages that isolate technical search data from creative branding to satisfy analytical decision-makers.

- Quantify the “Human” Element: Firms that lead with “human-centric” messaging (e.g., VOUS, H2A) must replace abstract promises with concrete performance metrics and localized case studies.

- Bridge the “Aesthetic-Technical” Gap: Agencies like Noosphere and Lola must pivot from “Magic” or “Meaning” to “Search Share” and “Market Demand,” explicitly linking brand aesthetics to search intent.

- Vertical Specialization: Instead of “Digital Agency,” firms are urged to become “Search Growth Architects” for high-value sectors such as Financial Services, Legal, or E-commerce.

Conclusion: Strategic Outlook

The Luxembourg SEO market is technically sound and geographically well-entrenched, but strategically stagnant. The industry is currently divided between “Full-Service Goliaths” who are too broad and “Creative Boutiques” who are too aesthetic.

The data concludes that technical proficiency is no longer a differentiator in Luxembourg; it is the “Floor.” The agencies that will dominate the next decade are those that can successfully productize their expertise and pivot their messaging from “Launching Websites” to “Scaling Organic Revenue.” Until the middle-tier agencies in Windhof and Bertrange stop listing services and start architecting market share dominance, they will continue to pay the “Genericity Tax” through lower margins and higher client churn. The path to leadership lies in owning the “Multilingual Technical” niche and proving clinical ROI in a market that values precision above all else.

Get Your SEO Strategy