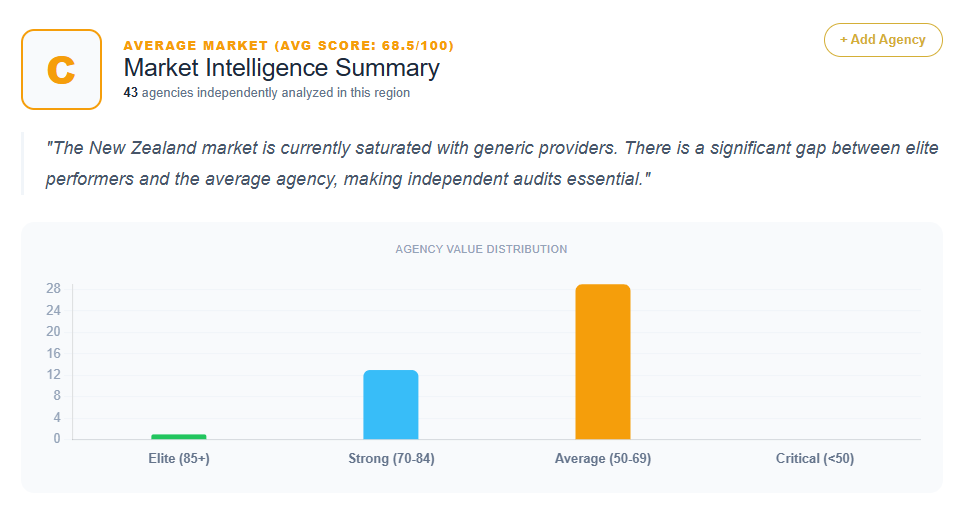

The digital marketing landscape in New Zealand presents a complex picture of professional competence frequently undermined by a lack of strategic differentiation. Analysis of 28 distinct SEO providers across the country—ranging from hyper-local boutiques in Whangaparaoa and Blenheim to high-tier performance engines in Auckland and Christchurch—reveals a market where technical fulfillment is high, but unique value propositions are rare.

Based on the quantitative data provided, agency scores span from a low of 58 (NetValue Ltd, Designit, and IdeaX) to a peak of 88 (King Kong). While many firms achieve “safe” scores in the mid-60s to low-70s, a recurring theme across nearly all diagnoses is the “Commodity Trap.” This describes a state where agencies rely on generic industry jargon like “results-driven,” “data-led,” and “ROI-focused,” which, while technically accurate, fail to distinguish them from hundreds of local and offshore competitors.

The Performance Spectrum: Analyzing the Scores

The New Zealand market is tiered into three distinct categories based on strategic maturity. At the top of the spectrum are the “High-Authority Performers” like King Kong (88) and Zyber (84). These agencies win because they either offer a massive “risk-reversal” (such as a guaranteed ROI model) or they pivot away from generalism toward high-stakes platform specialization, such as Shopify Plus growth engineering.

The middle market is the most crowded, featuring agencies like Found (78), Search Republic (78), and FWD (78). These firms are noted for high-quality branding and professional execution but are frequently penalized for “Institutional Genericness.” They are perceived as “safe bets” but often lack a distinct “Strategic Moat.”

The lower-tier scores (58 to 64) generally belong to firms suffering from “Generalist Dilution.” Agencies like NetValue Ltd (58) or Designit (58) often treat SEO as a secondary “bolt-on” service to software development or creative design. This lack of specialization creates a perception of SEO as a maintenance task rather than a core revenue engine.

Recurring Patterns: The “Commodity Trap” and “Strategic Anemia”

A dominant pattern across the NZ market is what one diagnosis calls “Strategic Anemia.” This is particularly visible in firms like ClickThrough (64) and See Me Media (62). Their value propositions focus on baseline industry standards, such as “measured results” or “getting noticed.” This positioning creates high friction because it fails to answer the fundamental client question: “Why this agency specifically?”

The Generalist Paradox

Many agencies, including Signify (68) and Fabric Digital (74), fall into the “Generalist Paradox.” They emphasize being “full-service” and “meaningful digital experiences.” While this builds brand affinity, it introduces significant friction in high-intent SEO acquisition. Sophisticated clients looking for algorithmic dominance may perceive these “creative-first” agencies as lacking the technical rigor required for high-stakes search campaigns. This “Aesthetic-Strategic Gap” is a recurring weakness where brand elegance is prioritized over a proprietary technical mechanism.

Geographic Pigeonholing

A significant number of agencies define themselves primarily by their geography. Christchurch SEO (62), Pogo (62, Hamilton-based), and See Me Media (62, Whangarei-based) rely on local trust signals. While this captures regional SME intent, it creates a “brand ceiling.” The data suggests that branding as a local utility rather than a strategic growth partner makes these agencies vulnerable to national players who lead with business intelligence rather than just technical implementation.

Technical vs. Commercial Positioning: The Authority Gap

There is a clear divide in how New Zealand agencies balance their technical expertise against their brand narrative.

The “Soul” vs. “The Science”

Flow (72) uses the proposition “Digital Marketing with Soul.” While unique, the analysis suggests this creates strategic misalignment by prioritizing emotional resonance over technical authority. Conversely, agencies like Zyber (84) or FWD (78) lean into performance metrics but are criticized for allowing their search-specific technical depth to be obscured by broader “growth” narratives.

The Lack of Proprietary Frameworks

One of the most frequent prescriptions across all 28 agencies is the need to “productize” the service. Most NZ agencies sell “SEO Services,” which is an interchangeable commodity. The market lacks “Signature Systems.” Prescriptions for firms like Responsive (68), Bluefusion (68), and Pogo (62) explicitly recommend naming their internal processes (e.g., “The Responsive Velocity System” or “The POGO Pulse Audit”) to move away from hourly-rate comparisons.

ROI Impact and the Financial Cost of Poor Differentiation

The lack of a sharp, differentiated value proposition carries a quantifiable financial toll. The provided ROI notes across the dataset suggest several recurring impacts:

- Lower Conversion Rates: Generic messaging for firms like Flow or NetValue Ltd likely leads to a 15-40% lower conversion rate on high-intent inbound leads.

- Extended Sales Cycles: For agencies like Vanguard 8 (76) and Adhesion (72), the lack of a “Strategic Hook” increases the time spent in the discovery phase by 15-20% as sales teams must manually explain differentiation that isn’t evident on the site.

- Price Sensitivity: When an agency is perceived as a commodity (e.g., Click and Convert, score 64), it is forced into price-based negotiations. This results in an estimated 25-35% lower Average Contract Value (ACV) compared to specialized growth partners.

- Revenue Leakage: Top-tier boutique agencies like FWD (78) may still experience a 15% revenue leakage because their messaging remains “safe” rather than “disruptive,” allowing more aggressive competitors to capture high-margin enterprise retainers.

Local Market Nuances and Cultural Calibration

The New Zealand market presents unique cultural challenges. The diagnosis for King Kong (88) highlights a fascinating “local market nuance”: their hyper-aggressive, Australian-centric branding can trigger “tall poppy” skepticism in the more reserved New Zealand business ecosystem. This suggests that “performance-guaranteed” models must be carefully calibrated to align with local business culture to avoid alienating risk-averse NZ enterprises.

Conversely, agencies like Rocketspark (74) leverage server proximity and NZ-localized support as a moat against global SaaS giants. However, they face an “Ease-of-Use Paradox,” where the simplicity of their tools leads users to believe SEO is a “set-and-forget” feature rather than a dynamic strategy, potentially capping the performance of scaling Kiwi brands.

Prescriptions for Market Leadership

To escape the “middle-market squeeze,” the data identifies three critical pivots for New Zealand agencies:

- Move from “Services” to “Systems”: Agencies are urged to rename their processes to create perceived intellectual property. Transitioning from “we do SEO” to “we utilize the [Branded] Framework” shifts the conversation from labor to value.

- Vertical Specialization: Instead of being “Auckland’s Best Agency,” firms are advised to become the “SEO Authority for NZ E-commerce” or “SaaS Growth Experts.”

- Quantified Outcomes: Replacing abstract claims of “growth” with specific financial metrics (e.g., “$XXM in organic revenue generated for NZ clients”) is essential for reducing sales friction and justifying premium pricing.

Conclusion: The Strategic Evolution of NZ SEO

The analysis of these 28 providers illustrates that while New Zealand possesses a high baseline of technical SEO competence, the industry is strategically stagnant. The average agency is professional and functional but “strategically quiet.”

The highest scores (84-88) are reserved for those who provide absolute clarity on ROI or extreme platform specialization. For the majority of the market scoring in the 60s, the path forward involves a radical decoupling from generic “results-driven” language in favor of proprietary mechanisms and quantified, sector-specific authority. Until these firms shift from being “vendors of tasks” to “architects of revenue,” they will remain trapped in price-sensitive competition, regardless of their technical rigor.

Get Your SEO Strategy