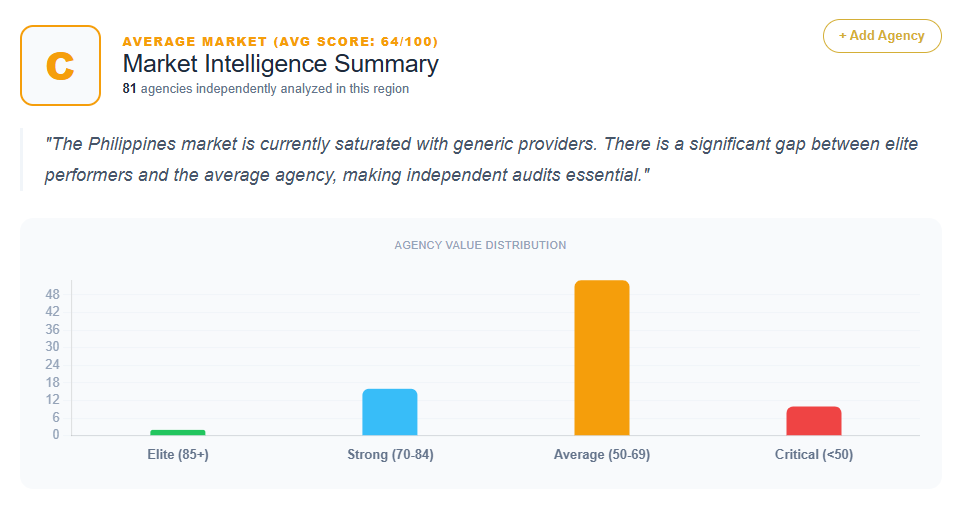

An exhaustive analysis of 81 SEO agencies and consultants currently operating in the Philippines reveals a market undergoing a difficult transition. While the country is a global powerhouse for operational execution and outsourcing, the diagnostic data shows that the majority of providers struggle to move beyond being “vendors of tasks” to becoming “architects of revenue.”

The performance scores in this dataset range from a high of 88 to a low of 25, highlighting a massive delta in strategic maturity. With a heavy concentration of providers scoring between 58 and 68, the Philippine market is currently saturated with “Safe Generalists”—firms that are technically competent but strategically invisible. For businesses seeking organic growth in the Philippines, the challenge is navigating a sea of providers that often treat high-stakes SEO as a clerical commodity rather than a performance-driven growth engine.

The Scoring Spectrum: A Numerical Evaluation of 81 Providers

The quantitative data provides a clear hierarchy of market authority. Out of the 81 agencies analyzed, the “Alpha Tier” is exceptionally thin. Propelrr leads the market with a score of 88, followed by Spiralytics at 86, and Growth Rocket at 84. These top-tier performers are distinguished by their focus on integrated lifecycle marketing and data-informed strategies. Close behind are OOM Philippines and MediaOne, both scoring 82, leveraging high-authority institutional trust and ISO certifications to differentiate from local boutique competitors.

However, the “Middle Market” is where the most intense competition occurs. Scores of 68 are shared by 15 different agencies, including Arma SEO, Sytian Productions, ExaWeb Solutions, and ReKreate Digital. This clustering suggests a “Sea of Sameness” where firms offer identical service lists—keyword research, link building, and on-page audits—without a proprietary methodology to justify premium pricing.

At the bottom of the spectrum, agencies scoring below 50, such as Digital Marketing Manila (48), Cebu Web Services (48), and EyeWebMaster (42), are frequently diagnosed with the “Commodity Trap.” These firms compete primarily on price and accessibility, leading to what the data describes as a “race to the bottom” that suppresses margins and results in high client churn.

The “BPO Identity Crisis”: Why Labor-First Models are Failing Strategic Clients

A recurring theme across the 81 agencies is the friction caused by the Philippines’ legacy as an outsourcing hub. Firms like Sourcefit (64), Worldhub Services (58), 2ndOffice (64), and Vintazk (62) represent the “BPO Model” of SEO. These agencies position SEO as a staffing commodity—selling “heads” rather than “growth.”

The ROI diagnosis for these firms is consistently negative regarding high-tier acquisition. For instance, Sourcefit is noted to capture 30-40% less revenue per client than specialized growth agencies because they sell “hours” instead of “outcomes.” Similarly, Worldhub and Right Job Solutions (42) treat SEO as a task-oriented BPO service alongside customer support, signaling to sophisticated buyers that they provide “hands but no brains.” The prescription for these agencies is universal: they must decouple their digital marketing identity from their general outsourcing brand to avoid “Generalist Dilution.”

The Specialist’s Myopia and the Generalist Trap

The data reveals two distinct strategic pitfalls that limit agency growth: “Specialist’s Myopia” and “Generalist Dilution.”

Specialist’s Myopia

SharpRocket (78) and ArrowUp Media (78) are recognized as world-class execution specialists, particularly in link building. However, their high scores are capped by a “strategic ceiling.” SharpRocket is diagnosed with messaging that is too siloed toward technical execution. By focusing on metrics like DR/DA rather than organic revenue, they miss out on full-service enterprise contracts. The data suggests that being an “agency’s agency” results in a 15-25% lower customer lifetime value (CLV) compared to firms that position themselves as a “CEO’s growth partner.”

Generalist Dilution

Conversely, the majority of mid-tier firms fall into the “Generalist Trap.” Agencies like NBK Consultancy (64), Brayne Digital (62), and iManila (62) try to be experts in everything from hosting and web design to PR and SEO. Sytian Productions (68) and UP Creative (68) prioritize aesthetics, making SEO a secondary “bolt-on” service. This dilution creates strategic friction; sophisticated B2B clients view these models as “shallow,” leading to a projected 25-35% loss in potential high-ticket revenue.

Geographic and Linguistic Barriers: The Failure of Foreign-Centric Models

The dataset includes several foreign agencies attempting to penetrate the Philippine market without localization. The results are numerically poor. LeadsLeader (25) is the lowest-scoring entry, largely because its German-language site creates a total cultural and linguistic barrier for PH businesses.

Similarly, Simply The Best Digital (42), MarketMind Local (42), and Webworks Digital (42) are penalized for “Western-centric” models. These agencies project generic growth claims while ignoring the mobile-first, social-commerce-integrated search landscape unique to the Philippines. The diagnosis for One Up Digital (62) highlights “Currency and Context Friction,” estimating that without a localized value prop, the agency likely leaves 30-40% of potential lead volume on the table.

Regional Powerhouses: Cebu, Davao, and the “Boutique Ceiling”

While Metro Manila remains the epicenter of competition, the analysis covers significant regional clusters:

- Cebu: Kapwa Marketing (72) and SEO Geniuses (62) show strong local relevance but are cautioned against “Transparency Hygiene” being their only USP. Cebu Web Services (48) and Cebu Web Solutions (52) are heavily penalized for focusing on “affordability,” which limits their scale to budget-conscious SMEs.

- Davao: Web Design Davao (42) and Kuya SEO (74) represent the two extremes of regional branding. Kuya SEO successfully leverages cultural trust through the “trusted brother” persona but hits a “Boutique Ceiling” due to a lack of enterprise-grade social proof. Web Design Davao, meanwhile, suffers from a dated aesthetic that contradicts its own service offering.

- Cagayan de Oro & Pampanga: Firms like Syntactics (68), Logicbase (62), and Brainnex (58) provide operational stability but are strategically quiet. Syntactics is noted for its “IT with a heart” cultural statement, which the data suggests obscures its ability to drive hard ROI for high-intent SEO buyers.

Prescriptions for Dominance: Productizing the Philippine SEO Offering

Across the 81 diagnoses, the most frequent prescription for growth is “Productization.” Almost every mid-tier agency is urged to rename their SEO process into a proprietary framework. Suggested names like “The SY-Scale Method,” “The Manila Velocity Framework,” or “The ARMA Velocity System” are proposed to move agencies from service-commodities to unique product owners.

The data indicates that shifting from “we do SEO” to “we utilize the [Proprietary] Framework” could reduce lead-to-close friction by 15-20%. Furthermore, agencies are advised to replace generic headers with “Impact Headlines” that quantify financial uplift (e.g., “Increasing Organic Revenue by X% for PH Retailers”) rather than listing technical tasks.

Local Market Nuances: The Missing Moat

The Philippine search market has specific nuances that many of the 81 agencies fail to exploit. Prescriptions for top-tier firms like Pure SEO (78) and OOM Philippines (82) emphasize the need to address “high-latency mobile environments” and “social-commerce dominance.”

The data suggests that the integration of SEO with local ecosystems like GCash, Maya, Lazada, and Shopee is a critical differentiator. Agencies that fail to mention these local infrastructure realities appear as “premium outsiders” or “corporate and detached,” which alienates local decision-makers who value relationship-driven results and hyper-local expertise.

Final Market Synthesis

The analysis of 81 Philippine SEO providers reveals a market with a solid technical floor but a hollow strategic middle. The industry is currently divided into three distinct zones:

- The Elite Stratosphere (82-88): Firms that sell business transformation and integrated data-science.

- The Competitive Middle (62-78): Professional firms that are indistinguishable from one another, paying a “Genericness Tax” in the form of lower conversion rates and longer sales cycles.

- The Commodity Floor (25-60): Firms and BPOs that compete on price and labor, suffering from high churn and thin margins.

For the majority of the market, the path to the 80+ tier requires a radical abandonment of generic marketing jargon. Until agencies in Quezon City, Makati, and the regional hubs productize their intellectual property and lead with revenue-first outcomes, they will remain trapped in price-sensitive negotiations, regardless of their technical capability. The Philippines is no longer just a source of “affordable hands”—to lead the market, agencies must prove they are a source of “strategic brains.”

Get Your SEO Strategy