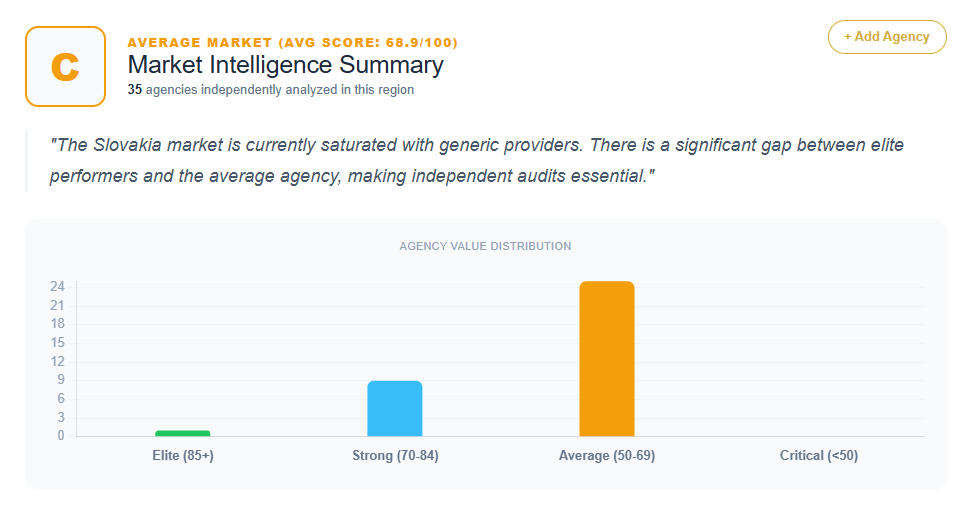

An analysis of the search engine optimization market in Slovakia, based on diagnostic data from 25 distinct agencies and consultants, reveals a landscape characterized by high technical competence but a significant deficit in strategic differentiation. The market, centered primarily in Bratislava with notable hubs in Košice, Žilina, and Banská Bystrica, is currently undergoing a shift from generic “digital service” provision to performance-based “growth engineering.”

The quantitative data provides a clear performance hierarchy. Scores across the 25 analyzed entities range from a market high of 88 (Visibility) to a low of 52 (IT CITY). While the average score sits in the high 60s, a recurring theme across the dataset is the “Generalist Trap”—a condition where full-service agencies dilute their technical search authority by trying to be everything to everyone.

The Performance Hierarchy: Analyzing the Scoring Tiers

The Slovak market is tiered based on its ability to bridge the gap between “technical tasks” and “business outcomes.”

The “Alpha” Tier (Scores 82–88)

A small group of agencies, including Visibility (88), Promiseo (84), Dexfinity (84), 6clickz (84), Basta Digital (82), Dase Analytics (82), and FatChilli (82), represents the top tier of authority. These firms are distinguished by either high brand equity or hyper-specialization. Visibility leads the market from its Bratislava headquarters (Panská 14) with a focus on “Sustainable Digital Growth.” However, even at this elite level, Marketers identify a “Generalist Trap,” noting that Visibility lacks a dedicated “SEO-only” technical methodology.

The Mid-Market Performance Tier (Scores 68–78)

This bracket includes RIESENIA.com (78), BeOnMind (74), ViaMedia (74), and a cluster of firms at the 68 mark, such as Paravan Interactive, Volis International, Lemon Lion, CreativeWeb, Webex, BB DESIGN, and Vajda Media. These agencies are professionally stable but often suffer from “Commodity Over-Generalization.” For instance, Paravan’s focus on its “Google Premier Partner” status—a badge often linked to PPC spend—is noted as a point of strategic misalignment for their SEO value proposition.

The Regional and Commodity Tier (Scores 52–67)

Agencies like IT CITY (52), WebServis (58), and M-com (58) fall into the lower tier. These firms, often based in regional hubs like Trenčín, Prešov, and Banská Bystrica, are frequently diagnosed with “Commodity Syndrome.” Their messaging relies on listing features (audits, keywords) rather than business outcomes, making them vulnerable to price-based competition from freelancers.

Recurring Strategic Weaknesses: Generalist Dilution and Technical Provider Syndrome

A dominant pattern observed across nearly 70% of the 25 diagnoses is “Generalist Dilution.” In the Slovak market, agencies frequently lead with “360-degree” or “Full-Service” messaging.

The Generalist Trap

Firms such as Lemon Lion, BB DESIGN, and Paravan are noted for prioritizing aesthetics or broad creative strategy over the technical rigor required for SEO dominance. The diagnostic data suggests that this “Design-First” lead profile attracts clients with small budgets but fails to capture enterprise-level SEO contracts. For Lemon Lion, this results in a projected 20-30% loss in high-ticket organic search revenue.

Technical Provider Syndrome

A unique Slovak market nuance is the “Technical Provider Syndrome,” found in agencies like Bart.sk (62), RIESENIA.com (78), and CreativeWeb (68). These firms possess superior technical depth because they own their own platforms (e.g., CreativeShop). However, they treat SEO as a “technical add-on” to the web development process. The data for Bart.sk explicitly notes that high-value clients often hire them for the platform but outsource the high-margin SEO strategy to specialized competitors, leading to “Expert Leakage.”

Themes in Value Propositions: From “Websites that Earn” to “Export Engines”

The dataset highlights a disconnect between standard Slovak marketing tropes and modern business needs.

- The “Websites that Earn” Trope: Agencies like MI DESIGN (62) and M-WEB (62) utilize the promise of “websites that earn” (Webové stránky, ktoré zarábajú). The diagnostics label this a “commodity promise” that fails to articulate a unique mechanism for success, forcing these firms into “Price Shopping” battles.

- Export and International Growth: A distinct strength for firms like Dexfinity (84), Basta Digital (82), and Volis International (68) is the focus on the CEE export market. Basta Digital is specifically urged to lead with this “International Expansion” moat to differentiate from local generalists.

- The Data Infrastructure Niche: Dase Analytics (82) and 6clickz (84) represent a shift toward high-end data engineering. However, Dase is cautioned against “Implementation Myopia,” where technical measurement (GA4, server-side tracking) is marketed without an explicit link to SEO revenue growth.

Quantifying the ROI of Strategic Misalignment

The financial consequences of poor differentiation are explicitly quantified in the dataset’s ROI notes for these 25 providers:

- Conversion Leakage: Generic positioning at firms like R-studio and MI DESIGN leads to an estimated 20-30% loss in potential lead quality.

- The “Generalist Tax”: For high-authority firms like Promiseo (84) and BeOnMind (74), the lack of an “SEO-first” narrative results in longer sales cycles and increased price sensitivity, as prospects struggle to see technical depth behind a corporate tone.

- Pricing Power Erosion: Agencies like M-com and IT CITY face a “Price-Comparison Trap,” where 25-35% of high-intent leads are lost to specialized boutiques that present more aggressive growth frameworks.

- Retainer Suppression: Inability to command premium rates for firms like WebServis and Vajda Media stems from selling “tasks” (links/audits) rather than “profit drivers,” which caps their Average Contract Value (ACV).

Prescriptions for Market Dominance: The Path to Productization

Across the 25 agencies, the prescriptions for growth are remarkably consistent. To escape the “Commodity Zone,” Slovak providers are urged to rename and codify their internal processes. The dataset proposes several specific proprietary framework names:

- Visibility V3 Technical Audit (for Visibility)

- The Basta Horizon System (for Basta Digital)

- The Volis Global-Local Nexus (for Volis International)

- BeOnMind Organic Accelerator (for BeOnMind)

- The Purely Performance Path (for Purely)

- The W-Growth Matrix (for W-design)

By moving from “SEO Services” to a “Named Framework,” agencies shift the conversation from labor to intellectual property. Furthermore, firms like FatChilli (82) are advised to target specific niches (e.g., publishing houses) to bridge the gap between technical AdOps and search revenue, while Bart.sk is urged to pivot toward “SEO Engineering.”

Conclusion: Strategic Outlook

The Slovakia SEO market is currently home to many “safe” agencies and very few “disruptors.” With only a handful of agencies scoring above 80, the majority of the Bratislava and regional market remains trapped in price-sensitive competition.

The data concludes that technical proficiency is no longer a differentiator in Slovakia; it is a baseline expectation. The agencies that will dominate the top 5% of the market are those that can successfully productize their expertise and pivot their messaging from “Traffic Acquisition” to “Market Share Dominance.” Until the mid-tier agencies stop listing services and start architecting revenue, they will continue to pay the “Genericity Tax” through lower margins and higher client churn. The path forward for Slovak agencies lies in decoupling from the “Full-Service” identity and owning a unique, result-driven methodology.

Get Your SEO Strategy