An exhaustive analysis of 45 SEO agencies and digital service providers currently operating in Slovenia reveals a market characterized by high technical competence but a significant deficit in strategic differentiation. Based on diagnostic data across firms in Ljubljana, Maribor, Celje, and regional hubs like Škorfja Loka and Murska Sobota, the industry is currently struggling with “Generalist Dilution.” While the technical floor of the industry is solid, only a small fraction of providers has successfully moved from being service vendors to strategic growth partners.

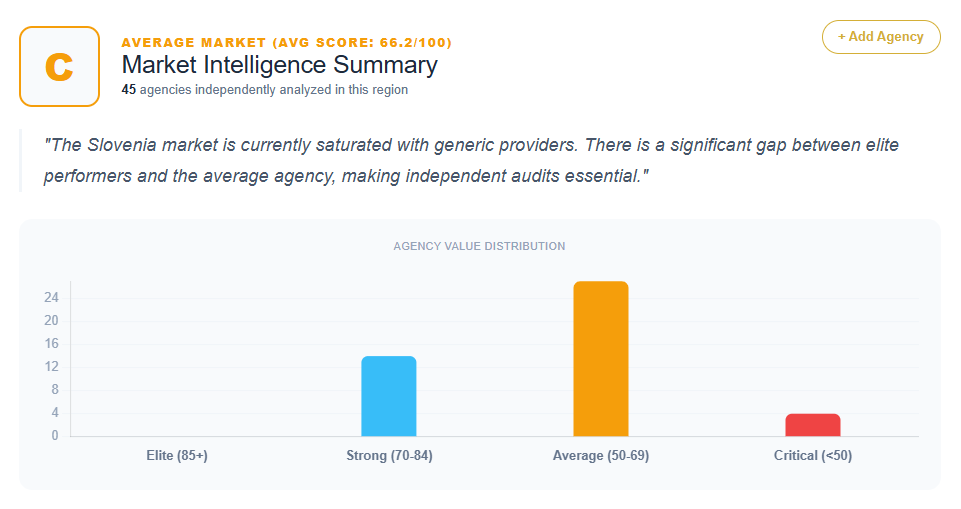

The quantitative data provided indicates a broad performance spectrum. Agency scores peak at 84 (Optiweb) and reach a low of 42 (E-poslovanje). A heavy concentration of scores resides between 62 and 68, representing nearly 40% of the analyzed group. This clustering suggests a market saturated with “Safe Generalists”—firms that are technically competent but strategically quiet, leading to significant revenue leakage and high price sensitivity.

The Performance Hierarchy: Analyzing the Scoring Tiers

The Slovenian SEO market is sharply tiered based on an agency’s ability to bridge the gap between “technical optimization” and “financial ROI.”

High-Authority Performers (Scores 80–84)

Only a handful of agencies, including Optiweb (84), Red Orbit (82), Dase Analytics (82), Inchoo (82), and Escape Digital Agency (82), represent the top tier of authority in Slovenia. These firms distinguish themselves through Google Premier Partner status, institutional credibility, or specialized technical niches. However, even at this level, the data notes a “Generalist Dilution” for Optiweb and “Academic Messaging” for Red Orbit, suggesting that even market leaders struggle to communicate visceral business outcomes over technical processes.

Mid-Market Contenders (Scores 70–79)

This segment includes Madwise (78), Dominatus (78), Point Out (78), Creatim (78), April 8 (78), Fokus (78), E-laborat (78), and high-performing boutiques like Upscale (74), Dotline (74), and Emigma (74). These agencies are professionally presented but are frequently diagnosed with “Strategic Neutrality.” The diagnosis for Upscale and April 8 highlights that “growth through digital marketing” has become a commodity statement, failing to distinguish their specific methodology from dozens of mid-market competitors.

Regional and Low-Tier Providers (Scores 42–69)

The lower tier includes regional generalists and legacy IT providers such as Spletne Storitve (48), Infocenter (48), Microteam (48), and Netcom (48). These firms are consistently diagnosed with “Strategic Misalignment.” In many cases, SEO is marketed as a secondary technical “add-on” to unrelated services like hardware maintenance, computer repair, or directory listings.

Recurring Strategic Weaknesses: The Generalist Trap

The most prevalent diagnosis across the 45 providers is the “Generalist Trap.” In the Slovenian market, agencies frequently lead with a “360-degree” or “Full-Service” narrative, which the data suggests is a primary cause of authority dilution.

Creative vs. Technical Misalignment

Agencies such as Zadrga (68), Studio 33 (68), and Dog and Pony (68) prioritize aesthetics, branding, and “storytelling.” While visually superior, this creates a “Strategic Misalignment” for clients seeking aggressive organic growth. The data suggests that without a clear performance-centric hook, creative agencies are often perceived as “too artsy” for technical search challenges, potentially costing them 20-30% in missed revenue.

IT Utility vs. Strategic Growth

Firms such as Megam (58), Microteam (48), and TRANS-IT (62) bundle SEO with infrastructure services like hosting and hardware. The diagnostic data for Microteam notes that grouping SEO with printer repairs fails to establish the authority required for premium SEO consulting. Similarly, Megam is noted for a “Strategic Dilution” where SEO is seen as a secondary technical add-on rather than a growth engine.

Patterns in Value Propositions: Descriptive vs. Outcome-Driven

The majority of Slovenian agencies rely on “Descriptive Functionalism.” This is evident in the messaging of firms like Net-it (62), Adis Digital (62), and M-WEB (62), which focus on SEO tasks—audits, keywords, and link building—rather than business outcomes.

The data identifies a recurring “Commodity Loop” in the Ljubljana hub. For instance, Dotcom (64) and W3B (68) are noted for “Commoditized Growth,” where their service descriptions are interchangeable with dozens of other agencies. Even agencies with strong niche positioning, like Inchoo (82) in e-commerce, suffer from “Technical Myopia,” leading heavily with platform expertise (Adobe Commerce) rather than market dominance results.

Regional Hub Analysis: Ljubljana vs. The Provinces

The physical location of an agency in Slovenia significantly influences its competitive positioning and strategic flaws:

- Ljubljana (The Competitive Epicenter): Home to Red Orbit, Madwise, Point Out, and others. Agencies here compete on “Institutional Credibility” but often pay a “Genericness Tax,” as prospects view them as interchangeable.

- Maribor & Celje (The Regional Challengers): Hub for Pro Marketing (68), Kreativna pika (68), and IT Melona (58). These firms often have high technical competence but suffer from “Strategic Stagnation.” Pro Marketing is noted for a transactional value prop that lacks the consulting narrative found in Tier-1 competitors.

- The Coastal & Western Hubs (Koper, Nova Gorica, Postojna): Agencies like Emigma (74) and M design (64) represent these regions. Emigma is noted for technical depth but falls behind in “Search-to-revenue” storytelling.

Local Market Nuances: Directory and Export Gaps

The dataset includes specific findings on how agencies navigate (or fail to navigate) the unique complexities of the Slovenian market.

Legacy Directory Models

Firms like Vsi.si (58) and Infocenter (48) are anchored in outdated directory-first models. Strategic misalignment occurs because these portals are emphasized as primary SEO levers, which conflicts with modern demands for standalone organic authority. The data predicts a conversion-killing effect for high-ticket B2B leads who perceive this as a lack of technical innovation.

The Export Opportunity

A distinct strength for firms like Dexfinity (84), Volis International (68), and Upscale (74) is the focus on cross-border growth and export into DACH markets. However, the data notes that for Volis, the failure to articulate a unique methodology for this export niche results in a “Commodity Over-Generalization.”

Quantifying the ROI of Strategic Misalignment

The financial consequences of poor differentiation are explicitly quantified in the dataset’s ROI notes:

- Lower Conversion Rates: Generic messaging for firms like Madwise and Red Orbit result in a projected 15-20% lower lead-to-close ratio. Prospects are forced to do the mental work to connect data to profit.

- Lead-to-SQL Friction: Agencies that do not quantify their impact through revenue-first messaging (e.g., Kontra, Point Out) experience an estimated 15-20% leakage in potential conversions.

- The “Commodity Tax”: For mid-tier firms like Adlab (68) and Signum (68), the lack of a “Strategic Hook” results in a 20-30% discount on potential retainers as clients default to price-based decision-making.

- Sales Cycle Inflation: For high-authority boutiques like Logit (82), the lack of a visceral hook results in sales cycles stretching to 6-12 months.

Prescriptions for Market Dominance: The Shift to Outcomes

Across the 45 agencies, the prescriptions for growth center on the transition from “what we do” to “how much the client earns.” To dominate the Slovenian market, agencies are urged to:

- Pivot to “Search-Led Revenue Growth”: Transition headlines from “SEO Services” to “Organic Market Share Domination” or “Revenue-First Search Strategy.”

- Isolate SEO Excellence: Decouple marketing services from IT maintenance (for firms like M-IT and Microteam) or directory listings (for Vsi.si) to build specialist authority.

- Inject Quantitative ROI: Move from creative jargon to hard metrics, such as “Average 140% organic growth for SI-retailers.”

- Vertical Specialization: Replace generic claims with niche dominance in high-value Slovenian sectors like Luxury Tourism, Export Manufacturing, or E-commerce.

Conclusion: The Strategic Evolution of Slovenian SEO

The analysis of these 45 providers indicates that the Slovenia SEO market is technically mature but strategically underdeveloped. The industry is home to “IT Generalists,” “Creative Shops,” and “Directory Portals,” but very few “Search Growth Architects.”

The data concludes that technical proficiency is no longer a differentiator in Slovenia; it is a baseline expectation. The agencies that will define the next phase of market leadership are those that can successfully decouple their marketing from generic jargon and lead with revenue-centric narratives. Until the mid-tier agencies in Ljubljana and Maribor stop listing services and start architecting revenue, they will continue to pay the “Genericity Tax” through compressed margins and high client churn. The path forward for Slovenian agencies lies in owning a unique, result-driven methodology that solves specific business growth bottlenecks.

Get Your SEO Strategy