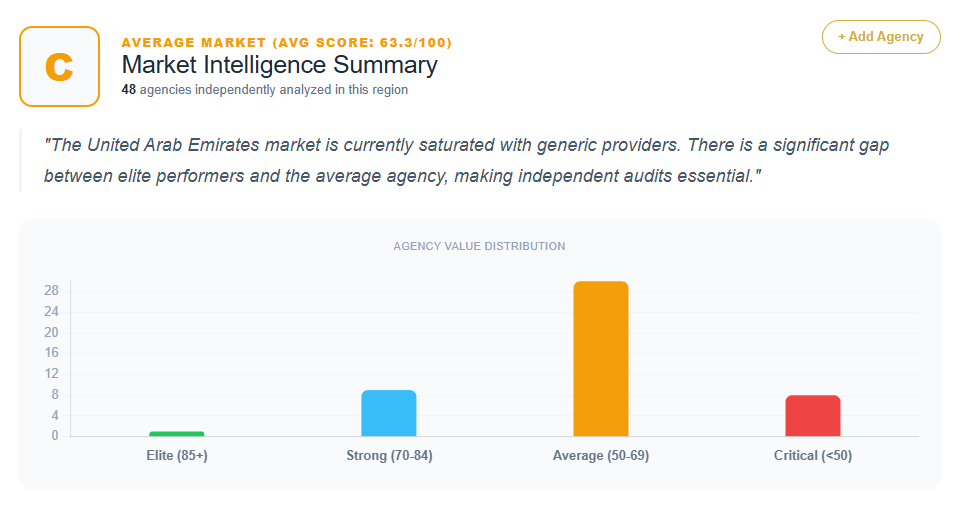

The United Arab Emirates’ search marketing sector is defined by high competitive density and a stark divide between elite strategic partners and commodity vendors. An analysis of 48 distinct SEO agencies operating across the UAE—from the high-authority towers of Business Bay and Jumeirah Lakes Towers (JLT) to regional players in Ras Al Khaimah and Sharjah—uncovers a market where technical competence is often overshadowed by strategic anonymity.

The quantitative data shows a massive performance spectrum. Scores range from a peak of 92 (SEO Sherpa) to a baseline of 42 (shared by Golden Falcon Advertising, Sonoma Infotech, NAT Web Solutions, and Pankaj Kumar SEO). With 48 agencies analyzed, patterns of “Generalist Dilution” and “Superlative Fatigue” are evident in over 60% of the dataset, suggesting that many firms are functional but strategically invisible.

The Performance Hierarchy: Quantifying Agency Authority

The scoring data establishes three clear tiers of service in the UAE.

The Elite and High-Authority Tier (Scores 76-92)

Only a handful of firms achieve elite status. SEO Sherpa (92) dominates the specialized organic space, though its diagnosis points to a 10-15% missed opportunity by not immediately leading with an “Arabic-first” hook. Digital Nexa (84) follows, winning on “CRM synergy” and its Elite HubSpot status, though it is penalized for burying its technical SEO methodology under broad “Growth” narratives.

Chain Reaction (78), SEO.ae (78), and Pivot Digital (78) represent the high-tier performance bracket. These agencies leverage significant social proof—such as Pivot Digital’s portfolio including Emaar and Majid Al Futtaim—but are often diagnosed with “Commoditized Excellence.” AAAA (76) and United SEO (76) also sit in this tier, though both are prescribed to move away from industry clichés like “ROI-focused” toward proprietary, named frameworks.

The Middle-Market and “Commodity Trap” (Scores 60-74)

The largest concentration of agencies resides in this bracket. House of Comms (74) and Global Media Insight (74) possess massive institutional stability, yet their SEO messaging is often secondary to their legacy in PR or 360-degree digital excellence. Firms like 7G Media (68), SEO Shark (68), and Beontop (68) suffer from “stagnant, feature-heavy messaging.”

Agencies in Business Bay, such as Si3 Digital (62), WebMedia (62), and Smart Vision (62), frequently mimic a “full-service” generalist model. This tier is defined by “Me-Too” positioning, where the lack of a unique selling proposition (USP) forces them to compete on price rather than strategic superiority.

The Lower-Tier and Offshore-Hybrid Model (Scores 42-59)

The bottom tier is characterized by “Strategic Anonymity” and a lack of regional presence. Sonoma Infotech (42) and NAT Web Solutions (42) are identified as offshore models that lack localized Middle Eastern market intelligence. Regional boutiques like RAK Digital (58) or Techcybers (48) are hindered by “Geographic Crutch Syndrome,” where their focus on a specific emirate signals a ceiling on their technical capabilities.

Recurring Strategic Weaknesses Across the Market

Across the 48 diagnoses, three primary friction points emerge: “Generalist Dilution,” “Superlative Fatigue,” and the “Bilingual Gap.”

Generalist Dilution and Identity Friction

A significant number of UAE agencies treat SEO as a modular add-on rather than a performance engine. BI Communications (62) and Golden Falcon Advertising (42) are primary examples where SEO specialization is secondary to PR or traditional printing legacies. This results in what the data calls “Generalist Fatigue.” House of Comms (74) is specifically noted for potentially losing $200k+ in annual specialized retainer revenue because search-specific leads perceive them as a “creative shop” first.

Superlative Fatigue

The data highlights a widespread reliance on unverified claims. Aspiration Worx (64), Beontop (68), and D Marketing (62) use generic descriptors like “Best SEO Agency” or “No. 1 Agency.” This triggers skepticism in the Dubai market, where enterprise-level prospects prioritize clinical ROI data over vanity superlatives.

The Bilingual (Arabic/English) Gap

Despite the UAE’s bilingual requirements, many agencies under-leverage Arabic SEO. Prescriptions for firms like SEO Sherpa, Bird Marketing (72), and Sweans Technologies (64) emphasize the need to move “Arabic-First” strategies to the forefront. Moris Media (64) and Digital Gratified (58) are penalized for using “global templates” that ignore GCC consumer behaviors and Middle Eastern search nuances.

Local Nuances and the Geographic Divide

The physical location of an agency in the UAE correlates strongly with its market positioning.

- Business Bay & JLT: This is the epicenter of high-intent search competition. Agencies like United SEO, Beontop, Upbeat Digital (64), Zen Ranking (68), and Blazon Solutions (64) are all clustered here. The result is “Comparison Fatigue” for prospects, as these agencies often present interchangeable value propositions.

- Sheikh Zayed Road: Firms like Global Media Insight (74) and Webology World (62) leverage these high-visibility addresses but are warned to move from “Legacy Dilution” to “Technical Transparency.”

- The Northern Emirates: RAK Digital (58) and Taqnia (48) struggle to compete for national enterprise contracts because their messaging is too localized to Ras Al Khaimah or focused on broader GCC targeting without Dubai-specific precision.

Quantifying the ROI of Strategic Misalignment

The financial impact of a non-differentiated value proposition is quantifiable across the dataset.

- Lead-to-Close Ratios: Agencies like Moris Media (64) or XCL Technologies (58) likely see a 20-30% reduction in lead conversion due to a perceived lack of specialization.

- Commodity Pricing: 10X Digital (64) and Upbeat Digital (64) are forced into price-sensitive sales cycles, potentially losing 20-30% in average retainer value compared to agencies with a unique “Growth Framework.”

- Wasted Marketing Spend: For offshore providers like Digital Gratified (58) or Pankaj Kumar SEO (42), the “Trust Gap” resulting from a lack of local social proof leads to a projected 35% lower conversion rate for UAE-based leads.

- Retention and Churn: Generalist positioning at firms like Pixel Media (58) or Digital Piloto (48) leads to higher client churn, as the service is viewed as an “interchangeable expense” rather than a strategic investment.

The Path to Dominance: Prescriptions for UAE Agencies

The dataset provides clear prescriptions to bridge these authority gaps:

- Productization: Nearly every mid-tier agency is advised to name their methodology. Whether it is “The Gulf Visibility Matrix” (SEO UAE), “The MENA Search Intent Protocol” (Chain Reaction), or “The Shark-Eye Analysis” (SEO Shark), moving from “service” to “system” is the primary driver of premium pricing.

- Vertical Specialization: Generalists like United SEO and Blazon Solutions are encouraged to highlight deep expertise in UAE-specific sectors like Real Estate, Luxury Retail, or Tourism.

- Arabic-First Focus: Firms like Sweans Technologies and Bird Marketing must move beyond English-centric SEO and elevate bilingual optimization to a core strategic pillar to capture regional enterprise demand.

- Clinical Social Proof: Agencies like Global Media Insight and GMI are prescribed to replace generic service descriptions with “Impact Headlines” that quantify historical revenue generation (e.g., “AED 50M+ Generated for UAE Clients”).

Conclusion

The analysis of these 48 UAE SEO providers reveals a market that is technically sound but strategically stagnant. While elite agencies like SEO Sherpa and Nexa have carved out high-authority moats, the majority of the Dubai and Abu Dhabi market remains trapped in a “commodity cycle.”

The ultimate differentiator in the 2024 UAE search landscape is no longer the ability to rank keywords, but the ability to articulate a unique, proprietary mechanism that links search visibility to business revenue. Agencies that continue to lead with “Full-Service” claims or “No. 1” superlatives will remain vulnerable to specialized boutiques that lead with clinical data, bilingual mastery, and sector-specific dominance. Until the middle tier of Business Bay and JLT firms productize their intellectual property, they will continue to pay the “Genericness Tax” through lower margins and higher acquisition costs.

Get Your SEO Strategy