Executive Summary

The Australian SEO market in 2026 is characterized by high maturity and significant technical baseline standards, yet it remains hindered by a “differentiation deficit” in the mid-market. While elite agencies command high authority through specialization and R&D, the majority of the landscape relies on defensive value propositions such as “no lock-in contracts” and “transparency.” The average score across the 33 evaluated agencies is 72.8, indicating a professionally sound market that is strategically stagnant. The defining insight for Australia is that while agencies are technically competent, they are trapped in a commodity cycle, competing on rapport and administrative flexibility rather than unique, proprietary growth mechanisms.

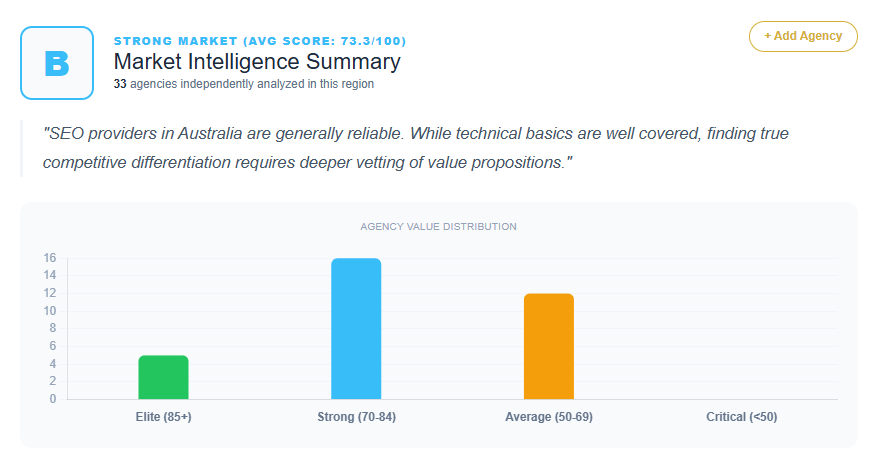

Market Maturity Score

- Average agency score: 72.8

- Score distribution:

- 80–92: 7 agencies (Brodie Clark Consulting, StudioHawk, DEJAN Marketing, Prosperity Media, Online Marketing Gurus, Bonfire, Scott Shorter)

- 70–79: 14 agencies (Engine Scout, Digital Hitmen, Supple Digital, Safari Digital, Advisible, Impressive, Kia Ora Digital, Margin Media, Luminary, BFJ Digital, Dilate Digital, Living Online, Frank Digital, Zib Digital)

- 60–69: 10 agencies (Noir and Blanco, Talons Marketing, Sixgun, MyWork Digital, Digital Nomads HQ, PWD Digital Marketing, Online Path, Digitally Up, JABA, Adelaide SEO Marketing)

- <60: 2 agencies (Top SEO Sydney, Direct Clicks)

- Market maturity classification: Mature but Undifferentiated

Differentiation Density

- % of agencies with proprietary frameworks: 0% (Every agency in the dataset is prescribed to codify or name a proprietary methodology, as none currently utilize a branded system.)

- % with vertical specialization: ~15% (Agencies like Kia Ora Digital focus on Shopify/eCommerce, and Prosperity Media focuses on Digital PR.)

- % with strong social proof: ~24% (High-authority signals are concentrated in the top-tier agencies with Deloitte Fast 50 or major industry awards.)

- % with unique mechanisms: 0% (The market relies on generic service delivery rather than branded intellectual property.)

Commodity Trap Index

- % using generic messaging: ~85% (Common usage of “results-driven,” “data-driven,” “transparency,” and “ROI-focused.”)

- % relying on service lists instead of outcomes: ~70% (Most agencies lead with a list of tactics—SEO, PPC, Social—rather than a unified strategic solution.)

- % with no unique mechanism: 100% (Prescriptions across all 33 audits highlight the absence of a named proprietary process.)

Top Agencies in Australia (By Score)

- Brodie Clark Consulting — 92

- StudioHawk — 92

- DEJAN Marketing — 88

- Prosperity Media — 88

- Online Marketing Gurus (OMG) — 88

Strengths of the Australia SEO Market

- Strong Technical Leadership: Top-tier agencies show a high commitment to R&D and technical auditing (e.g., DEJAN, StudioHawk).

- Client-Centric Risk Mitigation: Widespread use of “no lock-in contracts” across the mid-market to build trust.

- Operational Scale: Large national footprints with multiple physical offices are common among market leaders (e.g., Zib Digital, Supple Digital).

- High Visual and UX Standards: Agencies maintain professional, high-energy brand identities (e.g., Digital Hitmen, Noir and Blanco).

- Institutional Reliability: Established players leverage decades of experience and Google Premier Partner statuses.

Weaknesses of the Australia SEO Market

- Generalist Dilution: Most agencies offer a “360-degree” suite that thins their specialized SEO authority.

- Academic vs. Commercial Gap: High-end technical agencies often struggle to translate complex R&D into C-suite ROI narratives.

- Reliance on External Badges: Excessive dependence on awards and partner logos to substitute for a unique strategic methodology.

- Creative Over-Indexing: Design-heavy agencies often treat SEO as a secondary “add-on” rather than a performance driver.

- Superlative Fatigue: Frequent use of unverified claims like “#1 SEO Agency” leads to buyer skepticism.

ROI Impact Summary

- Estimated conversion loss: 15–30% (Driven by generic messaging and the failure to articulate a unique “How” behind the service.)

- Estimated ACV compression: 15–20% (Agencies are forced into price comparisons due to a lack of proprietary frameworks or “Expert Premiums.”)

- Estimated sales cycle extension: 10–20% (Procurement teams struggle to differentiate between top-tier specialists and mid-market generalists.)

Market Archetype Classification

High‑Authority but Low‑Differentiation

(The Australian market boasts immense technical talent and social proof, but the messaging is interchangeable across 85% of the evaluated firms.)

Sector Opportunities in Australia

- Underserved Verticals: Shopify/eCommerce specialization (Kia Ora Digital is a rare exception), Medical, Legal, and Technical B2B.

- Oversaturated Verticals: Generalist SME marketing, “Full-service” digital digital growth, and generic “results-driven” SEO for local trades.

Methodology

- Number of agencies: 33

- Scoring system reference: 0–100 scale evaluating value proposition, differentiation, and strategic alignment.

- Data source: Agency audits and competitive benchmarking (2026).

- Year: 2026

Related Pages

Get Your SEO Strategy