Executive Summary

The Estonian SEO market in 2026 presents a landscape characterized by high technical competence but significant strategic “Commodity Traps.” While the region is home to world-class technical providers and enterprise-level digital giants, the majority of agencies struggle to differentiate themselves, often relying on generic service descriptions rather than proprietary methodologies. With an average score of 64.26, the market is technically sound but suffers from a “Generalist Dilution” where SEO expertise is frequently buried under broader web development or IT umbrellas. A defining insight is the “Trust Tax” imposed on international providers lacking local physical presence or native Estonian linguistic authority, which significantly hampers their ability to capture domestic market share.

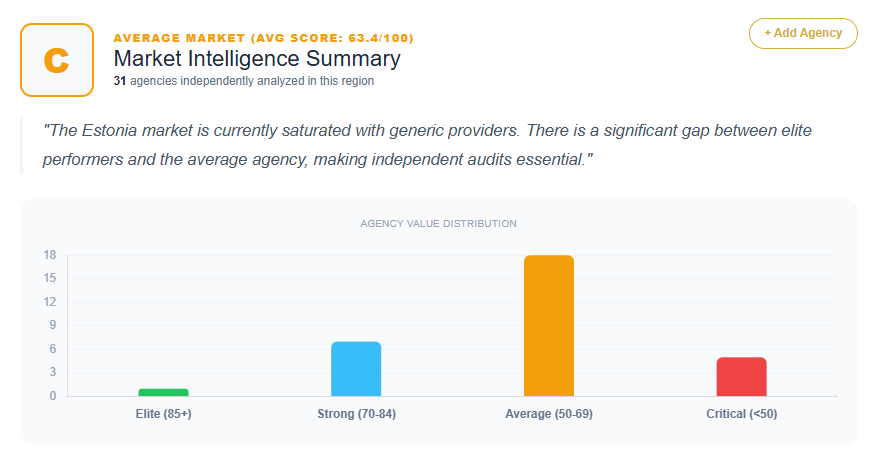

Market Maturity Score

- Average Agency Score: 64.26

- Score Distribution:

- 80–89: 3 agencies (Lavii, Editorial.link, Scandiweb)

- 70–79: 5 agencies (Blumint, Xysum, ADM Interactive, SEOBRO, Zgraya Digital)

- 60–69: 15 agencies (Delante, Links-Stream, Renua, Redhornet, Molivery, Wunderplan, IT-Agentuur, Artmedia, Veebiarendus, Mediaberry, Tulemus, Smart Marketing, Digiagentuur, Veebidisain, SEO-teenused.ee)

- <60: 8 agencies (Ethical SEO, Vahid SEO, Digiturundus.ee, Kodulehe Tegemine, Pärnu SEO, Kohtla-Järve Veeb, Ida-Viru Turundus, Marketing Expert)

- Market Maturity Classification: Saturated Generalist Market

Differentiation Density

- % of agencies with proprietary frameworks: ~10% (Only a few leaders like Lavii and Scandiweb leverage unique strategic systems; most are prescribed to develop one.)

- % with vertical specialization: ~13% (Specializations identified include SaaS/Unicorns at SEOBRO, E-commerce at Scandiweb, and elite backlink procurement at Editorial.link.)

- % with strong social proof: ~16% (Limited to top-tier local firms like ADM Interactive, Lavii, and Scandiweb; most mid-tier agencies are criticized for lacking visible Estonian case studies.)

- % with unique mechanisms: ~6% (Most agencies focus on technical deliverables rather than unique, named delivery mechanisms.)

Commodity Trap Index

- % using generic messaging: ~81% (Recurring themes of “data-driven,” “results-oriented,” and “growth-focused” messaging across 25+ evaluated agencies.)

- % relying on service lists instead of outcomes: ~77% (Agencies like Renua, IT-Agentuur, and Artmedia focus on deliverables such as “on-page/off-page” rather than ROI or revenue architecture.)

- % with no unique mechanism: ~84% (The majority of the market lacks a “Signature System,” leading to brand invisibility in a crowded field.)

Top Agencies in Estonia (By Score)

- Lavii Digital Marketing Agency — Score: 86

- Editorial.link — Score: 84

- Scandiweb — Score: 84

- ADM Interactive — Score: 76

- SEOBRO — Score: 74

Strengths of the Estonia SEO Market

- High Technical Ceiling: Agencies like ADM Interactive and Scandiweb leverage deep engineering and DevOps backgrounds for superior technical SEO.

- SaaS Ecosystem Alignment: Specialized players like SEOBRO and Blumint are highly optimized for the “Tallinn Hub” and the local startup/unicorn culture.

- Strong Local Presence: The presence of physical headquarters in Tallinn (e.g., Lõõtsa and Pärnu mnt clusters) provides a “local trust factor” that is essential for domestic dominance.

- E-commerce Expertise: Dominant regional players offer high-tier full-stack engineering for global e-commerce growth.

Weaknesses of the Estonia SEO Market

- Generalist Dilution: SEO value propositions are frequently lost within all-in-one IT, hosting, or web design service bundles.

- Linguistic and Regional Gaps: International agencies often lack native Estonian linguistic authority and understanding of the specific .ee search landscape.

- The “Regional Trap”: Agencies based in smaller cities (e.g., Pärnu, Kohtla-Järve) struggle with perceived scale and technical depth compared to Tallinn firms.

- Aesthetic Over Performance: Several boutique firms prioritize “Impactful Design” over measurable search growth and technical ROI signals.

ROI Impact Summary

- Estimated Conversion Loss: 15–30% for agencies with generic messaging, rising to 60–70% for international firms lacking localized trust signals.

- Estimated ACV Compression: Mid-tier agencies lose an estimated 15–25% in contract value by competing on price-sensitive “commodity” keywords rather than value-driven engagements.

- Estimated Sales Cycle Extension: Lack of proprietary methodologies and unique “hooks” forces longer education phases in the sales funnel, as prospects view agencies as interchangeable.

Market Archetype Classification

Saturated Generalist Market — The Estonian landscape is crowded with professional, technically competent agencies that offer near-identical service menus, leading to high “Comparison Fatigue” for potential clients.

Sector Opportunities in Estonia

- SaaS and Tech Exports: High-value niche for agencies that can translate local success into global organic visibility.

- Bilingual Search Dominance: Underserved opportunity for agencies that can master both Estonian and Russian search intent in the Baltic corridor.

- Technical SEO for Enterprise Migrations: A gap exists for agencies that can weaponize high-end engineering skills specifically for SEO-led digital transformations.

- E-Residency Support: Targeting international brands entering the Baltics via Estonia’s digital infrastructure.

Methodology

- Number of Agencies: 31

- Scoring System Reference: Proprietary 100-point scale evaluating value proposition, localization, and market differentiation.

- Data Source: Strategic agency audits conducted in the Estonian market.

- Year: 2026