Executive Summary

The SEO market in Indonesia is characterized by a high volume of established players with strong institutional trust, yet it remains largely hindered by a “Generalist Trap.” With an average maturity score of 66.48 across 31 evaluated agencies, the market is professionally stable but strategically stagnant. Most firms position SEO as a secondary add-on to web development or creative services, leading to significant brand dilution. While a few elite technical specialists are emerging in Jakarta, the majority of the market competes on price and generic “page 1” promises rather than proprietary frameworks or quantified business outcomes.

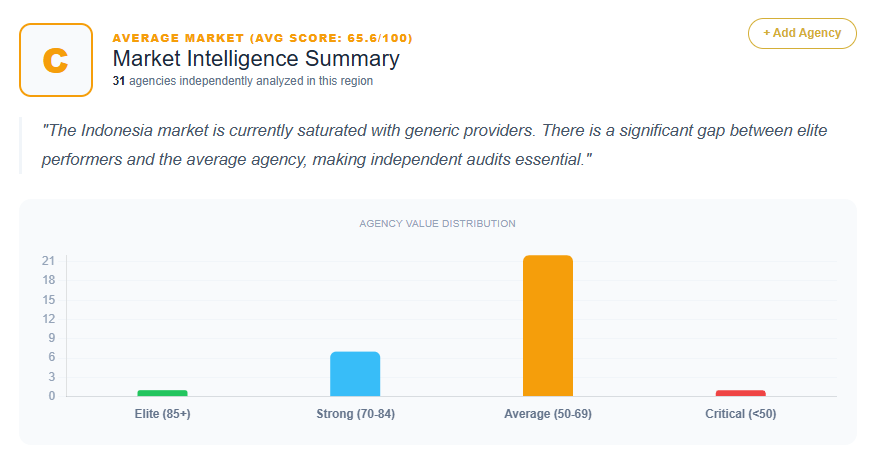

Market Maturity Score

- Average Agency Score: 66.48

- Score Distribution:

- 80–89: 1 Agency (cmlabs)

- 70–79: 7 Agencies (LOGIQUE, Redcomm, Seven Ads, ToffeeDev, Arfadia, Meson Digital, Urala Communications)

- 60–69: 14 Agencies (Walden, Enterpage, Island Media, Next Digital, CREF, Surabaya SEO, Levelon Digital, Tomato Digital, DI Marketing, Iman Iawan, Reezh Design, SEO Team, Ideoworks, LimeCommerce)

- <60: 9 Agencies (DGtraffic, Fruitech, SEO Medan [Score 58], Medan SEO, SEO Medan [Score 56], Nurhasan, Peter & Co., DibalikSEO, PageTraffic)

- Market Maturity Classification: Saturated Generalist Market

Differentiation Density

- % of agencies with proprietary frameworks: ~3% (Only cmlabs demonstrates a clear tech-enabled ecosystem; most others are prescribed to develop one).

- % with vertical specialization: ~19% (Specializations noted in hospitality/Island Media, e-commerce/LimeCommerce, and regional niches in Surabaya and Medan).

- % with strong social proof: ~16% (Blue-chip portfolios noted for agencies like Redcomm, Meson Digital, and LOGIQUE).

- % with unique mechanisms: ~3% (The vast majority rely on standard service lists rather than unique technical methodologies).

Commodity Trap Index

- % using generic messaging: ~90% (Common usage of “trusted,” “best,” “data-driven,” and “results-oriented” without proprietary backing).

- % relying on service lists instead of outcomes: ~87% (Focus on deliverables like backlinks and articles rather than revenue or market share growth).

- % with no unique mechanism: ~97% (Fail to distinguish their technical process from the standard industry baseline).

Top Agencies in Indonesia (By Score)

- cmlabs (Content Marketing Labs) | Score: 87

- LOGIQUE Digital Indonesia | Score: 78

- Redcomm Indonesia | Score: 74

- Seven Ads Indonesia | Score: 74

- ToffeeDev | Score: 74

Strengths of the Indonesia SEO Market

- High Institutional Trust: Many agencies hold ISO certifications and Google Premier Partner statuses, signaling high operational compliance.

- Strong Physical Presence: Most providers maintain verified physical offices in major economic hubs like Jakarta (Kuningan, Menteng), Surabaya, and Medan.

- Technical Development Foundation: A significant portion of the market consists of hybrid IT/Development shops with deep internal knowledge of site architecture and technical builds.

- Regional Dominance: Strong local authority exists in specific provinces (East Java, North Sumatra), allowing for hyper-local search targeting.

Weaknesses of the Indonesia SEO Market

- Generalist Dilution: Agencies frequently group SEO with unrelated services like PR, video production, and web design, weakening their perceived technical authority.

- Activity-Based Narrative: Messaging is heavily “feature-centric” (we do X) rather than “outcome-centric” (we achieve Y revenue).

- Lack of Localized Strategic Depth: Many firms fail to address Indonesia-specific digital behaviors, such as the dominance of the Tokopedia/Shopee ecosystem or mobile-first search nuances.

- Stagnant Value Propositions: A reliance on 2018-era “ranking-first” models that fail to satisfy modern, data-driven CMOs.

ROI Impact Summary

- Estimated Conversion Loss: Agencies suffer from a 20% to 45% leakage in potential enterprise leads due to generic positioning and a lack of specialized “clinical” authority.

- Estimated ACV Compression: Failure to differentiate forces agencies into “Price Wars,” depressing Average Contract Value by an estimated 15% to 40% compared to specialized consultants.

- Estimated Sales Cycle Extension: The “Trust Gap” created by dated UI/UX and non-differentiated messaging leads to longer consideration phases and higher cost-per-acquisition for new clients.

Market Archetype Classification

Saturated Generalist Market

The Indonesian landscape is crowded with “full-service” providers. While technical competency is high, strategic differentiation is low, creating a market where most agencies are viewed as interchangeable commodity vendors.

Sector Opportunities in Indonesia

- E-commerce Revenue Optimization: Moving beyond simple traffic to focus on Direct-to-Consumer (DTC) revenue in a marketplace-dominated economy.

- Technical SEO for Enterprise Scale: High demand for agencies that can handle Core Web Vitals and complex architectures for Indonesia’s growing SaaS and FinTech sectors.

- Local E-E-A-T Specialization: Developing content strategies that address the specific linguistic and cultural nuances of the Indonesian searcher.

- Performance-Integrated Search: Bridging the gap between Paid Ads data and Organic SEO to create a unified “Search Intelligence” offering.

Methodology

- Number of Agencies: 31

- Scoring System Reference: Based on 0-100 scale evaluating Value Proposition, Strategic Alignment, Differentiation, and ROI signaling.

- Data Source: Independent audit of Indonesian digital marketing and SEO agency digital footprints.

- Year: 2026