Executive Summary

The Saudi Arabian SEO market in 2026 is characterized by a significant transition from traditional digital marketing to a more sophisticated, localized performance landscape. While the market shows high potential, it is currently hampered by “Generalist Syndrome,” with an average agency score of 63.3. Out of 30 agencies evaluated, a majority struggle to move beyond generic service descriptions to offer the technical and cultural depth required by the Kingdom’s “Vision 2030” digital transformation. The defining market insight is the critical trust gap between offshore/generalist providers and the rising demand for “Arabic-First” technical SEO strategies tailored to Saudi consumer behavior.

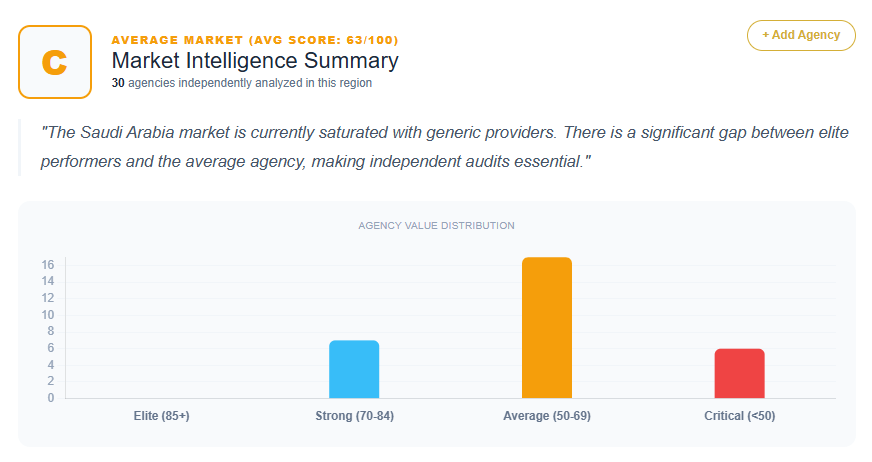

Market Maturity Score

- Average Agency Score: 63.3

- Score Distribution:

- 80–89: 0 agencies

- 70–79: 7 agencies

- 60–69: 17 agencies

- <60: 6 agencies

- Market Maturity Classification: Emerging but Fragmented

Differentiation Density

- % of agencies with proprietary frameworks: 0% (Most evaluations explicitly prescribe the development of a unique mechanism, as current offerings are viewed as commoditized).

- % with vertical specialization: ~10% (Only a small subset focuses on specific sectors like government giga-projects, retail, or real estate).

- % with strong social proof: 23% (Primarily the top-tier agencies with verified Riyadh offices and local client portfolios).

- % with unique mechanisms: 0% (Agencies rely on standard industry tropes rather than branded, defensible methodologies).

Commodity Trap Index

- % using generic messaging: 93% (Terms like “results-driven,” “data-driven,” and “creative excellence” dominate the landscape).

- % relying on service lists instead of outcomes: 87% (Most agencies focus on “what” they do—SEO, PPC, Social—rather than “why” it matters for Saudi market share).

- % with no unique mechanism: 100% (The dataset indicates a systemic failure to productize SEO services into proprietary systems).

Top Agencies in Saudi Arabia (By Score)

- Chain Reaction – 79

- Novi Marketing – 78

- DPS (Digital Performance Solutions) – 76

- Affinity – 74

- Zarief – 74

Strengths of the Saudi Arabia SEO Market

- Strong Local Presence: A high concentration of agencies in Riyadh (Al Olaya and Al Malqa districts) ensures cultural alignment and “boots-on-the-ground” authority.

- Bilingual Capabilities: Leading agencies successfully navigate the dual-language (Arabic/English) requirements of the GCC search landscape.

- Professional Visual Identity: High-tier local agencies exhibit superior branding and UI/UX compared to offshore competitors.

- Vision 2030 Alignment: Agencies are increasingly framing digital transformation in the context of national economic goals to build institutional trust.

Weaknesses of the Saudi Arabia SEO Market

- Generalist Dilution: SEO is frequently positioned as a secondary creative service rather than a technical growth engine.

- Offshore Misalignment: International agencies (specifically from Turkey, India, and Australia) suffer from a lack of localized Arabic search data and cultural nuance.

- Linguistic Gaps: Failure to optimize for specific Saudi dialects (Najdi vs. Hejazi) leads to missed opportunities in high-intent local search.

- Generic Performance Claims: A reliance on “award-winning” or “ROI-driven” cliches without providing data-backed, sector-specific case studies.

ROI Impact Summary

- Estimated Conversion Loss: 15-35% reduction in lead conversion efficiency for agencies failing to localize their value proposition for the Saudi market.

- Estimated ACV Compression: The “Commodity Trap” forces agencies to compete on price, likely leading to a 20-50% lower average contract value compared to specialized regional leaders.

- Estimated Sales Cycle Extension: Trust friction and the lack of “Wasta” (local social proof) increase the cost per acquisition (CPA) by 20-25% and lengthen the sales cycle for non-localized firms.

Market Archetype Classification

- Emerging but Fragmented

Sector Opportunities in Saudi Arabia

- E-commerce Optimization: Specialized SEO for local platforms like Salla and Zid is currently underserved.

- Giga-Project Support: Technical SEO tailored for government-linked entities and Vision 2030 initiatives.

- Bilingual Search Authority: Hyper-localized content strategies focusing on Saudi-specific search intent and regional dialects.

- Vertical Specialization: High-growth sectors such as Real Estate, Fintech, and the Saudi retail sector remain dominated by generalists.

Methodology

- Number of Agencies: 30

- Scoring System Reference: 100-point Value Proposition Audit

- Data Source: Specialized KSA Agency Audits

- Year: 2026