Executive Summary

The Singapore SEO market in 2026 is characterized by high professional execution and a strong reliance on local authority signals, yet it remains hindered by widespread strategic sameness. While many agencies demonstrate high-tier market presence and technical competence, the majority fall into a “Commodity Trap,” offering nearly identical “results-driven” value propositions. The market is heavily influenced by local trust markers, such as physical CBD presence and PSG grant eligibility, creating a protective barrier for incumbents while simultaneously stifling unique strategic innovation. With an average score of 66.17 across 29 evaluated firms, the market represents a high-performing but undifferentiated landscape where “bespoke” strategies are frequently overshadowed by “biggest” claims.

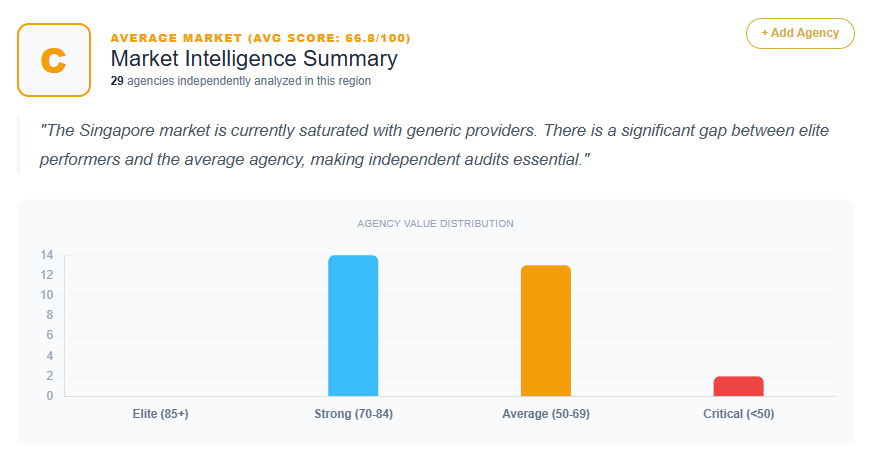

Market Maturity Score

- Average Agency Score: 66.17/100

- Score Distribution:

- 80–89: 1 Agency

- 70–79: 13 Agencies

- 60–69: 8 Agencies

- <60: 7 Agencies

- Market Maturity Classification: Saturated Generalist Market

Differentiation Density

- % of agencies with proprietary frameworks: 0% (Most agencies rely on generic descriptors; prescriptions across the dataset emphasize the need to develop named methodologies like “Alpha Growth Engine” or “Velocity Framework” to escape commodity pricing).

- % with vertical specialization: 17.2% (Agencies specifically targeting B2B Tech, FinTech, Web3, or Executive Reputation).

- % with strong social proof: 31% (Agencies leveraging high-authority client portfolios, Google Premier Partner status, or extensive local awards).

- % with unique mechanisms: 0% (Strategic “anonymity” and “anemia” are cited as primary frictions, with agencies lacking proprietary tech or LLM-based content workflows).

Commodity Trap Index

- % using generic messaging: 79% (Widespread use of “data-driven,” “results-oriented,” “ROI-focused,” and “full-service”).

- % relying on service lists instead of outcomes: 62% (Messaging prioritized “what we do” over specific “economic impact” or “unique mechanisms”).

- % with no unique mechanism: 100% (Every agency evaluated received a prescription to develop a branded, proprietary framework to distinguish their technical execution from competitors).

Top Agencies in Singapore (By Score)

- MediaOne Marketing: 82

- Found: 78

- Primal Digital Agency: 78

- Impossible Marketing: 78

- OOm Pte Ltd: 78

Strengths of the Singapore SEO Market

- High Institutional Trust: Market leaders maintain deep credibility through Google Premier Partnerships, ISO certifications, and verified physical presences in the CBD (e.g., Robinson Road, Tras Street).

- Government Integration: A significant segment of the market leverages the PSG (Productivity Solutions Grant) as a primary hook, lowering the barrier to entry for SMEs.

- Regional Footprint: Many agencies use Singapore as a “Gateway to SE Asia,” positioning themselves as regional powerhouses for brands looking to expand across APAC.

- Visual and Aesthetic Professionalism: High scores were consistently awarded for professional presentation and minimalist, sophisticated design-led growth narratives.

Weaknesses of the Singapore SEO Market

- Strategic Anonymity: A pervasive “Safety in Numbers” approach where agencies claim to do exactly what everyone else does, just “better” or “bigger.”

- TLD and Geographic Friction: Non-local entities (using .my domains or lacking physical offices) suffer significant trust deficits and “offshore” stigmas.

- Credential Inflation: An over-reliance on awards and partner badges that have become baseline expectations, leading to “Comparison Fatigue” among prospects.

- Linguistic Barriers: Agencies operating in non-English languages are categorized as having total market irrelevance for the domestic Singaporean landscape.

ROI Impact Summary

- Estimated Conversion Loss: 15–25% for agencies failing to differentiate their technical mechanism, as prospects default to price-based comparisons.

- Estimated ACV Compression: 25–40% loss in potential retainer value for agencies that position themselves as grant-supported vendors rather than high-tier strategic growth partners.

- Estimated Sales Cycle Extension: Significant friction for sophisticated buyers results in longer decision cycles as agencies fail to provide a “Category-of-One” reason for selection.

Market Archetype Classification

- High-Authority but Low-Differentiation

Sector Opportunities in Singapore

- Underserved Verticals: B2B SaaS, FinTech-specific SEO, and Executive Branding for APAC leaders are identified as high-value niches with low specialized competition.

- Technical Opportunities: Advanced “Edge SEO,” proprietary LLM-based content workflows, and ROI-centric “Revenue Intelligence” frameworks represent significant gaps in the current agency offerings.

- Oversaturated Verticals: Generalist SME digital marketing and grant-subsidized SEO services are highly commoditized, leading to lower margins and higher churn.

Methodology

- Number of agencies: 29

- Scoring system reference: Proprietary value proposition audit measuring strategic alignment, local authority, and unique mechanism presence.

- Data source: 2026 Singapore Agency Audit Dataset.

- Year: 2026