Executive Summary

The Swedish SEO market is characterized by high technical maturity and a strong culture of transparency, yet it is currently plagued by “Established Leader Inertia.” While the majority of agencies demonstrate high competency and professional standards, the market has reached a saturation point where “results-driven” and “data-driven” messaging have become the industry baseline. This has created a landscape of “Average Excellence,” where top-tier firms struggle to differentiate their execution from one another. To succeed in this sophisticated market, agencies are increasingly required to move beyond tactical SEO and adopt proprietary methodologies that align directly with C-suite objectives like EBITDA growth and market share dominance.

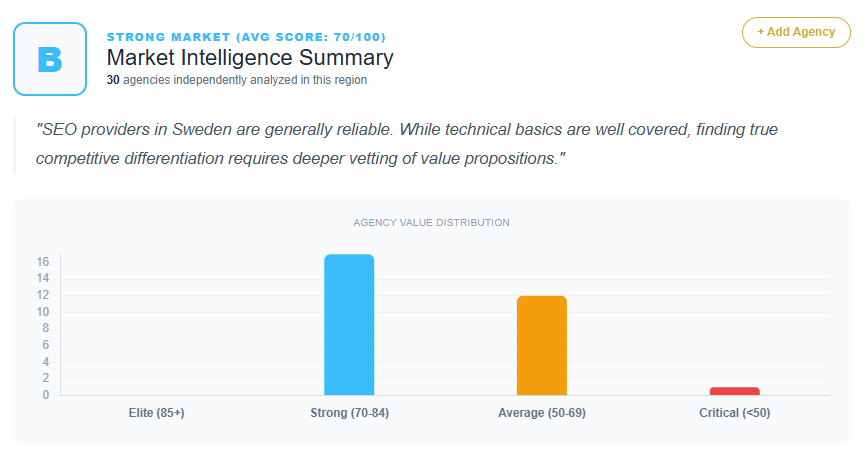

Market Maturity Score

- Average Agency Score: 69.6

- Score Distribution:

- 80–89: 2 agencies (Topdog SEO, Pineberry)

- 70–79: 15 agencies (Brath AB, Awisee, Viva Media, Keybroker, Raqs SEO-byrå, Noon, Sunbird, Be Better Online, Genero, Mild, Resultify AB, Nordic Morning, Semantiko, Wasabi Web, The Generation)

- 60–69: 11 agencies (Adrelevance, Pigment Webbyrå, SEO-doktorn, GoodOld, Webb of Sweden, Impera, Digiplant AB, Inkreo, Högst upp, WDM, Mediakoncept i Sverige AB)

- <60: 2 agencies (Västerås Webb, Pardott)

- Market Maturity Classification: High‑Authority but Low‑Differentiation

Differentiation Density

- % of agencies with proprietary frameworks: 6.6% (Only Topdog SEO and Pineberry exhibit clearly defined internal processes that approach a “unique mechanism,” though most others are prescribed to create one.)

- % with vertical specialization: 16.6% (Notable specialists include Awisee in iGaming, Awisee in International Link Building, and Pigment or The Generation in WordPress-specific SEO.)

- % with strong social proof: 23.3% (High-authority signals are concentrated in market leaders like Pineberry, Brath, Topdog, Wasabi Web, and Viva Media.)

- % with unique mechanisms: 3.3% (Topdog SEO is the primary outlier with its “Industrialized SEO” process.)

Commodity Trap Index

- % using generic messaging: 90% (Terms such as “results-driven,” “data-driven,” “digital growth,” and “visibility” are used by nearly all evaluated agencies.)

- % relying on service lists instead of outcomes: 83.3% (Most agencies lead with a menu of SEO, SEM, and Social Media rather than quantifiable business breakthroughs.)

- % with no unique mechanism: 93.3% (The vast majority of the market relies on brand equity and “transparency” rather than a named, proprietary methodology.)

Top Agencies in Sweden (By Score)

- Topdog SEO: 84

- Pineberry: 82

- Brath AB: 78

- Noon (Noon Digital Marketing AB): 78

- Sunbird: 78

- Wasabi Web: 78

Strengths of the Sweden SEO Market

- High Technical Competence: Most agencies possess a solid technical foundation, particularly in WordPress integration and performance marketing.

- Transparency and Trust: A legacy of transparent reporting is a standard expectation across the Stockholm and regional markets.

- Localized Expertise: Strong understanding of the Swedish search landscape, language nuances, and domestic consumer behavior.

- Integrated Service Models: Many agencies successfully bundle SEO with web development, SEM, and broader digital growth strategies.

Weaknesses of the Sweden SEO Market

- Strategic Anonymity: A prevalence of “me-too” messaging makes it difficult for clients to distinguish between mid-tier and high-tier providers.

- Service-Provider Mindset: Agencies often position themselves as tactical vendors rather than high-level strategic growth partners.

- Generalist Dilution: A tendency to offer “full-service” digital marketing often weakens the perceived depth of specialized SEO authority.

- Complexity Friction: High-end agencies occasionally lean too heavily on technical processes (the “How”) while neglecting the immediate business impact (the “Why”).

ROI Impact Summary

- Estimated Conversion Loss: 15–25% (Due to “Comparison Fatigue” and generic value propositions failing to resonate with performance-obsessed CMOs.)

- Estimated ACV Compression: 10–20% (Agencies are often forced into price-based “beauty contest” RFPs rather than value-based pricing.)

- Estimated Sales Cycle Extension: 15–20% (A lack of a unique “hook” or proprietary methodology requires manual proof of expertise during discovery, slowing down the sales process.)

Market Archetype Classification

- High‑Authority but Low‑Differentiation: The market is dominated by highly competent, professional agencies that suffer from “Institutional Genericness,” where their services are high-quality but strategically interchangeable.

Sector Opportunities in Sweden

- Revenue-First Technical SEO: Moving away from “rankings” to “EBITDA-focused” outcomes.

- Niche Dominance: Specializing in Swedish E-commerce growth, B2B SaaS, or the international scaling of Nordic brands.

- Productized SEO Services: Developing and naming proprietary frameworks (e.g., “The [Agency] Growth Engine”) to move away from commoditized service lists.

- WordPress/SEO Hybrid Authority: Leveraging technical development backgrounds to solve complex Core Web Vitals and indexing issues.

Methodology

- Number of agencies: 30

- Scoring system reference: 0–100 scale based on value proposition clarity, strategic differentiation, and market positioning.

- Data source: Comprehensive audits of established Swedish digital and SEO agencies (2025-2026).

- Year: 2026