Executive Summary

The Swiss SEO market in 2026 is characterized by high technical proficiency and professional reliability, but it suffers from extreme strategic homogeneity. With an average score of 64.6 across 30 evaluated agencies, the market is technically sound yet largely trapped in a “Full-Service” narrative. Most agencies rely on the “Swiss Quality” label as a baseline rather than a differentiator, leading to a landscape of interchangeable generalists. A few elite players demonstrate enterprise-grade sophistication, but the majority of the market is currently vulnerable to price-sensitive competition due to a lack of proprietary methodologies and vertical-specific specialization.

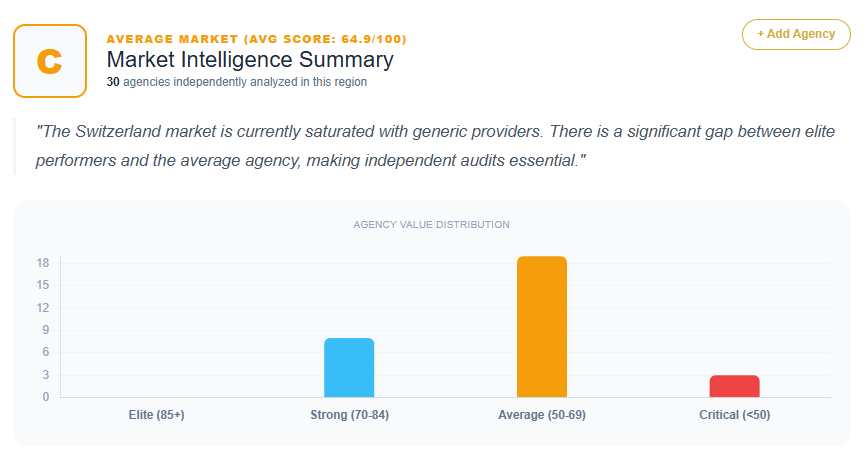

Market Maturity Score

- Average Agency Score: 64.6

- Score Distribution:

- 80–89: 1 agency (Webrepublic AG)

- 70–79: 7 agencies (BlueGlass Interactive AG, ProWeb Consulting, Darwin Digital, xeit GmbH, Zumo GmbH, SEO Native GmbH, Enigma)

- 60–69: 17 agencies (Netgen Switzerland, NinjaPromo, SEO Zürich, Dartera GmbH, FlinkThink GmbH, Firegroup AG, Fire8, Simba Digital, SEOX, SEO & Marketing GmbH, Agence eBiz, LPA, Online Marketing Basel, Agence Référencement, SEO Lausanne, Berner SEO, Top SEO)

- <60: 5 agencies (Shark Agency, ThatWare LLP, Nuwizo, Web Design Basel, Web-Agentur-Bern.ch)

- Market Maturity Classification: Saturated Generalist Market

Differentiation Density

- % of agencies with proprietary frameworks: 0% (The dataset indicates a systemic lack of named proprietary optimization frameworks, with most “prescriptions” recommending their development).

- % with vertical specialization: 10% (Only 3 out of 30 agencies, such as NinjaPromo for Fintech/SaaS, ProWeb for Enterprise, and LPA for Local SME search, show distinct vertical positioning).

- % with strong social proof: 23% (Only top-tier firms like Webrepublic, BlueGlass, and Darwin Digital are noted for having authoritative, data-driven narratives and enterprise-level social proof).

- % with unique mechanisms: 0% (Nearly all agencies are penalized for a lack of a “Mechanismic USP,” focusing on what they do rather than a proprietary “how”).

Commodity Trap Index

- % using generic messaging: 87% (26 out of 30 agencies rely on tropes like “Swiss Quality,” “visibility,” “data-driven,” or “transparent results”).

- % relying on service lists instead of outcomes: 90% (The majority of diagnoses highlight “Service-Feature Syndrome” or “Generalist Dilution,” where agencies list SEO as a sub-service among others).

- % with no unique mechanism: 100% (The dataset explicitly identifies the lack of a “proprietary growth engine” or “unique methodology” as a primary friction point across all evaluated entities).

Top Agencies in Switzerland (By Score)

- Webrepublic AG — Score: 82

- BlueGlass Interactive AG — Score: 78

- ProWeb Consulting — Score: 78

- Darwin Digital — Score: 76

- xeit GmbH — Score: 74

Strengths of the Switzerland SEO Market

- Technical Rigor: High baseline of technical competence and “Swiss-made” quality standards.

- Geographic Proximity: Strong local presence in key hubs like Zurich, Geneva, Basel, and Bern.

- Multilingual Potential: Innate market awareness of linguistic complexities (DE/FR/IT), though often underutilized as a USP.

- Compliance Standards: High reliability regarding data privacy (FADP/GDPR) and professional ethics.

Weaknesses of the Switzerland SEO Market

- Strategic Homogeneity: Excessive reliance on the “Full-Service” generalist model.

- Lack of Proprietary IP: Absence of named, branded methodologies that create perceived uniqueness.

- Clinical/Conservative Messaging: Brand voices often lack aggressive performance narratives or disruptive “Growth Partner” positioning.

- Service-First Focus: Messaging tends to describe tactical activities (audits, rankings) rather than financial business outcomes.

ROI Impact Summary

- Estimated Conversion Loss: 15–30% (High-intent leads frequently compare agencies on price due to lack of differentiation).

- Estimated ACV Compression: 20–40% (Generalist positioning forces agencies into price-sensitive procurement rather than value-based pricing).

- Estimated Sales Cycle Extension: Significant friction is noted as sophisticated clients struggle to distinguish “strategic alpha” between identical-looking service palettes.

Market Archetype Classification

- Saturated Generalist Market

Sector Opportunities in Switzerland

- Swiss Finance & Private Banking: Targeted search intelligence for high-net-worth acquisition.

- Luxury & Watchmaking: Specialized SEO for international Swiss-brand dominance.

- Pharma & MedTech: Technical SEO for highly regulated life science sectors in Basel and Zurich.

- Multilingual Search Authority: Explicit “Linguistic Growth” frameworks bridging German, French, and Italian search landscapes.

Methodology

- Number of Agencies: 30

- Scoring System Reference: Proprietary performance audit (0–100 scale)

- Data Source: Verified agency audits (2025–2026)

- Year: 2026